|

Source: Streetwise Reports 11/03/2020 The noteworthy points for investors about Nomad Royalty Company are presented in a BMO Capital Markets report.In an Oct. 12 research note, analyst Rene Cartier reported that BMO Capital Markets initiated coverage on Nomad Royalty Company Ltd. (NSR:TSX; NSRXF:OTCQX) with a Market Perform rating and CA$1.70 per share target price. Nomad's stock is currently trading at about CA$1.27 per share. Cartier described Nomad. It is a Montreal-headquartered precious metals-focused royalty and streaming company with a growing portfolio of assets, in North America, South America, Africa and Australia. Nomad was formed through a reverse takeover transaction and vend-in of two royalty and stream portfolios from Orion Finance and Yamana Gold. Those two companies own significant Nomad interests today. Nomad emerged with assets that are producing and generating cash flow and another one slated to come online this year. Subsequently, its management team made additional royalty/streaming acquisitions in more favorable jurisdictions to diversify its holdings. The company plans to actively expand its asset portfolio, mostly focusing on smaller deals and capitalizing on its credit facility and refinancing in the market through equity. It remains open to larger transactions, too, for which it would pursue "teaming up and syndicating deals with peers or alternative groups" to carry those out, Cartier explained. Financially, Nomad had about $12 million in cash on its balance sheet and no debt as of June 30, 2020. Today, in addition to cash, it has a $50 million revolving credit facility, which it could increase to $75 million. The analyst highlighted that Nomad's management team members are experienced and have strong track records in the royalty/streaming space. Each of the three co-founders, Vincent Metcalfe, Joseph de la Plante and Elif Levesque, previously worked for Osisko Royalties. One of management's goals is to decrease its annual general and administrative expense to somewhere in the $4–5 million range. "Management are not planning to take a cash salary for the first year, thereby aligning the success of their equity holdings along with other shareholders," noted Cartier. He also pointed out that Nomad, despite being a young company, pays, on a quarterly basis, the highest annual dividend ($0.02 per share) among its peer group. This is one way the company can return cash to shareholders, which is one of its goals. Finally, Cartier wrote that BMO believes that Nomad's stock is trading in line with its most comparable peers, which indicates that its portfolio is already significantly derisked. However, he added, that "establishing a performance track record, improving trading liquidity and portfolio diversification, and enhancing asset visibility will be of significance for Nomad Royalty." Read what other experts are saying about: Disclosure: Disclosures from BMO Capital Markets, Nomad Royalty Company, October 12, 2020 IMPORTANT DISCLOSURES Analyst's Certification Analysts who prepared this report are compensated based upon (among other factors) the overall profitability of BMO Capital Markets and their affiliates, which includes the overall profitability of investment banking services. Compensation for research is based on effectiveness in generating new ideas and in communication of ideas to clients, performance of recommendations, accuracy of earnings estimates, and service to clients. Analysts employed by BMO Nesbitt Burns Inc. and/or BMO Capital Markets Limited are not registered as research analysts with FINRA. These analysts may not be associated persons of BMO Capital Markets Corp. and therefore may not be subject to the FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. Company Specific Disclosures

( Companies Mentioned: NSR:TSX; NSRXF:OTCQX, ) from https://www.streetwisereports.com/article/2020/11/03/coverage-initiated-on-new-royalty-company-with-cash-flow-starter-pack.html

0 Comments

Source: Matt Badiali for Streetwise Reports 11/02/2020 Independent financial analyst Matt Badiali profiles two companies that he believes are poised to take off.The biggest commodity story in the last two years must be the gold price. It was just $1,200 per ounce in November 2018 and it broke $2,063 per ounce earlier this year. That's a 72% move in a fundamental commodity. As you can imagine, that drove the big gold producers up even higher. Over that same two-year period, the NYSE Gold Bugs Index (HUI) rose from 138 to 363. That's a 163% gain:

As you can see in the chart above, the index sagged a bit since August 2020. That's due in part to lower gold prices and to investors taking profits. I still think we'll get another shot at making money in the majors, when gold moves higher. But right now, I'm looking down the sector for the best opportunities. That's because some great companies missed the run up. There are a handful of small cap miners that offer a big reward for a little more risk. There are two that stand out. They were going through transitions in 2020, so they missed the big move in mining stocks. The first is Heliostar Metals Ltd. (HSTR:TSX.V; RGCTF:OTC). This company is the product of a merger between Redstar Gold Corp and Heliodor Metals Ltd. Its CEO is rising star Charles Funk. Charles and I share a love for high-grade gold projects. He thinks Heliostar has a good one in the Unga Project in Alaska. This is a brownfields project at the old Apollo Mine. It closed in 1922. There are multiple occurrences of bonanza grade gold and silver in several locations across the project. As of October 22, the company has three drill rigs on site. We can expect news soon. The company also has a portfolio of projects in Mexico, called Cumaro, Oso Negro and La Lola. These are early stage, epithermal targets with high-grade potential. The reason I like Heliostar, aside from management and projects, is that it is cheap right now. The timing of the merger meant that they missed the bulk of the run up in gold and gold stocks. At just C$40.5 million this company has enormous potential. There are companies with far less going for them that trade at three or four times that. I feel the same way about U.S. Gold Corp. (USAU:NASDAQ). This company also just completed the acquisition of Northern Panther Resource Corporation in August 2020. The corporate wrangling came at exactly the wrong time. As all the other junior gold miners soared, they were locked in negotiations. They didn't put out a press release from June 3 to August 12. That low profile is our opportunity today. The company owns the promising CK Gold project in Wyoming. It's a copper/gold deposit at surface that new President George Bee believes will make a great, profitable gold mine. U.S. Gold has three other prospective projects—Challis Gold in Idaho, Maggie Creek on the Carlin Trend in Nevada and Keystone on the Cortez Trend in Nevada. Both Challis and CK Gold have resource estimates. The company put out an updated preliminary economic estimate in March 2020. It showed that at $1,600 per ounce gold price and $2.80 per pound copper price, CK Gold had a net present value (NPV) of $321 million. That's more than ten times U.S. Gold's current market cap. I'd much rather buy that kind of opportunity than speculate on stocks that have already tripled or quadrupled in value. Most of those stocks are ripe for profit taking… But shares of Heliostar and U.S. Gold haven't even started to move yet. These are some of the best risk-reward setups I've seen in junior mining. --Matt Badiali Matt Badiali is a geologist and independent financial analyst. He spent fifteen years researching and writing about great investments inside the natural resources sectors. He can be reached at www.mattbadiali.net. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsStreetwise Reports Disclosure:

( Companies Mentioned: HSTR:TSX.V; RGCTF:OTC, USAU:NASDAQ, ) from https://www.streetwisereports.com/article/2020/11/02/these-two-overlooked-junior-gold-miners-offer-great-risk-reward-set-ups-right-now.html Source: Maurice Jackson for Streetwise Reports 11/02/2020 In this conversation with Maurice Jackson of Proven and Probable, the CEO of Rover Metals describes "high-grade" assays from three holes, and believes more positive results from the company's drill program will follow later in November.Maurice Jackson: Joining us for a conversation is Judson Culter, the CEO and director of Rover Metals Corp. (ROVR:TSX.V; ROVMF:OTCQB). Always a pleasure to have you back on our program to provide us with an update on the 2020 drill program on the historical high-grade Cabin Lake Gold Project. But before we begin, Mr. Culter, who is Rover Metals, and what is the opportunity the company presents to the market?

Judson Culter: Rover Metals is a precious metals exploration company. We're focused on advancing our existing gold assets, which are located in northern Canada. And the opportunity to the market is we're days away from releasing the remainder of our summer-fall drill program. I would say roughly 70% of the results are still to come, and that should be in the near term. Maurice Jackson: Absolutely. And speaking of the Cabin Lake Gold Project, Rover Metals embarked on an exploration drill program this summer on nine holes. Was the objective to twin the historical high-grade intersects?

Judson Culter: It was, but not identical twinning in terms of just going right next to the hole. We were just twinning an area, the high-grade area of the Bugow iron formation at Cabin Lake. And that's going down dip, and also coming at the drilling from different angles. And that includes leaving it in the mineralization until it's the hanging wall on the footwall. So really, it's not just textbook twinning. There is step-out exploration here. Maurice Jackson: Good to hear. The company just released the first three assay results on the exploration drill program. What can you share with us, sir?

Judson Culter: The results were great. No one has been there in 30 years. Historically, they used a much smaller core size. So there was, of course, going to be deviation, and just most likely a lesser drill rig than 30 years ago. So we learned about how to follow the high-grade on the first three holes. It was the second hole that we learned a lot about the deviation of the historical drilling. And we were able to correct the remainder of the drill program, namely holes three to nine, based on what we learned from hole two. And in doing so, we did stay and achieve our target holes.

I'll talk about the grades from the first hole. We had a long-intersect, continuous gold grades of 22 meters, and the average grams per ton (g/t) on that was 8 g/t. But certainly, there were some spikes as high as 46 g/t on smaller intervals. And then hole three—which is again, after we'd learned about the deviation from hole two—a similar story, where we found another large intersection of the high grade that we were chasing. That was roughly 6.5 g/t over 15 meters on that hole three. And when we pulled the core—we've logged all the core for the entire program—we knew what to look for. It's this iron formation that is highly sulfidized. So, I'm pretty confident to say that the best is yet to come on this drill program. Maurice Jackson: The company just answered an unanswered question. Were these the results that Rover was anticipating? Judson Culter: I think that the surprise has been the length of this economic grade of gold. I mean the historical drilling, the longest intersect was about 15 meters. So, we're well above that now and learning a lot more about how to chase the folding of this iron formation, which is where the high grade is located. Maurice Jackson: When should shareholders expect to receive the assay results on holes four through nine? Judson Culter: I would expect within the next couple of weeks; mid-November. We did two batches of samples. So the second batch of samples, which is holes four to nine, is at the lab, and they're prepping it. So I think we should be in pretty good shape here for mid-November. Maurice Jackson: Sounds good. Switching gears, Mr. Culter, please provide us with an update on the capital structure for Rover Metals. Judson Culter: Rover Metals has 77 million shares outstanding and roughly 15 million warrants, and those warrants have a strike price at $0.12. Maurice Jackson: What is the burn rate right now? Judson Culter: The burn rate is, I would say, outside of the exploration program that we just finished—let's go with $50,000 a month outside of the exploration season. Maurice Jackson: And how is the treasury looking right now? Judson Culter: Treasury is great. Once we pay for this drill program, we should still have about $150,000 in the bank. And we'll be looking for new financing sometime either the end of Q4/20 or early Q1/21. Maurice Jackson: In closing, Judson, why is this the perfect time to become a shareholder of Rover Metals? Judson Culter: Well, I think we've seen a little bit of come-off in gold, but the forecast for 2021 and 2022 is it's going to continue to be a very strong and healthy gold price. And we're just really in the right timing in terms of that gold cycle. We're hoping to be able to get an Inferred resource here, after this drill program. If one looks at the mining life cycle, we're in that part of the mining life cycle that can add the most shareholder value, which is this discovery to the potential. . .over the next three years, grow to an economic mine deposit. That's the cycle of investment that you're seeing with Rover Metals. Now is the time to get in, really—before the resource continues to grow in size. Maurice Jackson: Sir, what keeps you up at night that we don't know about? Judson Culter: My next interview with Proven and Probable, but that's okay. After today, we've got probably a couple of more weeks. Maurice Jackson: Last question, sir. What did I forget to ask? Judson Culter: In terms of business development, we're working on a few things right now in the background, and if that continues in the direction that it seems to be headed, might be able to have some news for the market here, as well in the coming weeks. Maurice Jackson: Mr. Culter, if investors want to get more information about Rover Metals, please share the contact information. Judson Culter: Just visit our website at www.rovermetals.com and visit the Contact Us page. Maurice Jackson: Mr. Culter, thank you for joining us today, and wishing you and Rover Metals the absolute best, sir. As a reminder, I'm a licensed broker for Miles Franklin Precious Metals Investments where we provide unlimited options to expand your precious metals portfolio, from physical delivery, offshore depositories, and precious metals IRAs. Call me directly at (855) 505-1900 or you may email [email protected]. Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure: Disclosures for Proven and Probable: Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734. The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk. Images provided by the author.

( Companies Mentioned: ROVR:TSX.V; ROVMF:OTCQB, ) from https://www.streetwisereports.com/article/2020/11/02/explorer-reports-drill-results-on-canadian-prospect.html Source: Streetwise Reports 11/02/2020 Shares of AngloGold Ashanti Ltd. traded 9% higher after the company reported that Q3/20 free cash flow increased 290% YoY to $339 million allowing it to double its dividend payout ratio to 20%.Global gold mining company AngloGold Ashanti Ltd. (AU:NYSE; ANG:JSE; AGG:ASX; AGD:LSE) today announced that in the third quarter of 2020 ended September 30, 2020, it delivered a 290% increase in free cash flow. The firm stated that the improvement in cash flow has helped bring down its adjusted net debt to the lowest level in almost 10 years, which it advised supports the decision to double its dividend payout ratio. AngloGold Ashanti reported that "it will pay shareholders 20% of its free cash flow before accounting for capital expenditure in growth projects, up from 10% previously." The company additionally indicated that going forward it will now pay dividends on semi-annual basis rather than annually. AngloGold Ashanti's Interim CEO Christine Ramon commented, "We will continue to enforce capital and cost discipline to deliver strong cash flows in this elevated gold price environment...Doubling our dividend payout ratio demonstrates confidence in our ability to both improve direct returns to shareholders and to self-fund our growth projects and sustaining capital requirements." The company stated that in Q3/20, free cash flow increased by 290% to $339 million, compared to $87 million in Q3/19. The firm said this was attributable to lower capital expenditure and operating costs and a 30% higher gold price received. AngloGold Ashanti noted that $200 million of the $329 million was derived proceeds from the sale of its South African operating assets to Harmony Gold on September 30, 2020. The company added that in Q3/20, cash inflow from operations increased by 56% to $551 million, compared to $354 million in Q3/19. AngloGold Ashanti reported that adjusted net debt was cut by nearly 50% to $875 million as of September 2020. The firm stated that in Q3/20 adjusted EBITDA increased by 72% to $803 million, compared to $468 million in Q3/19. The company listed that in the three months ended September 30, 2020, it produced 837,000 ounces of gold at a total cash cost of $801 per ounce, versus 825 Koz Au at a total cash cost of $786 per ounce in the prior year's corresponding quarter. The firm added that in Q3/20, all-in sustaining costs (AISC) were $1,044/oz Au, compared to $1,031/oz Au in Q3/19. The firm advised that it reinstated its annual guidance on September 21, 2020. AngloGold Ashanti stated that for FY/20, the company expects gold production of between 3.03 and 3.10 million ounces, which includes nine months of production from the recently sold South African operations. Excluding the South Africa assets, it estimates full-year production will range from 2.80-2.86 Moz Au on a continuing operations basis. FY/20 AISC is expected to come in at $1,060-1,120/oz, including contributions from the South African assets to the end of September 2020, and $1,050-1,100/oz Au on a continuing operations basis. AngloGold Ashanti Ltd. is headquartered in Johannesburg, South Africa, and according to the firm's website it is the third largest global gold producer and largest such firm in Africa, employing more than 34,000 people worldwide. The company indicated that its 2019 gold production exceeded 3.3 million ounces. The firm operates projects in nine countries including the Democratic Republic of the Congo, Ghana, Guinea, Mali and Tanzania in Africa, Australia, Argentina, Brazil and Colombia. The company is primarily a gold miner but also produces silver and sulfuric acid as by-products at some of its sites. AngloGold Ashanti has a market capitalization of around $9.6 billion with approximately 416.6 million shares outstanding. AU shares opened 7.5% higher today at $24.88 (+$1.74, +7.52%) over Friday's $23.14 closing price. The stock has traded today between $24.46 and $25.36 per share and closed at $25.28 (+$2.14, +9.25%). Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure:

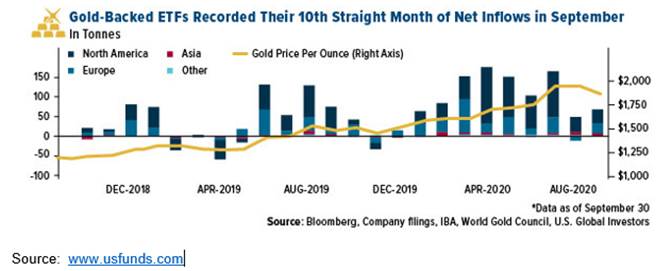

( Companies Mentioned: AU:NYSE; ANG:JSE; AGG:ASX; AGD:LSE, ) from https://www.streetwisereports.com/article/2020/11/02/anglogold-ashanti-doubles-dividend-payout-ratio-as-q3-free-cash-flow-increases-290.html Source: Peter Krauth for Streetwise Reports 11/02/2020 Peter Krauth explains why he believes gold will be the biggest winner in the election.There's no shortage of prognostications or conjecture about the U.S. election. Of course, everyone has an opinion. Some like red, some like blue, some like neither. Last week's volatility in stocks, bonds, currencies and commodities is a clear signal that markets are uneasy. They hate uncertainty. If the election's outcome is less than clear, then volatility will be around for a while, and probably even intensify. A lot of the forecasting is about what will happen to gold. One thing I know for sure is, no matter who takes election victory, gold will come out of it the biggest winner. In the meantime, we're likely to hear a lot of noise. I suggest you ignore most of it, and focus on the prize: soaring gold prices. Near-Term Gold Pressure Gold is already up 25% year-to-date. But that doesn't mean there's no gas left in its tank. Here are the main drivers influencing the gold price. I see two temporary headwinds for gold. The first is central banks. Bloomberg reported recently that "central banks became gold sellers for the first time since 2010, as some producing nations exploited near-record prices to soften the blow from the coronavirus pandemic." The World Gold Council (WGC) said Q3 saw central banks (CBs) become net sellers of 12.1 tons versus last year's net buying of 141.9 tons. Russia was a standout, with its first net sales in 13 years as oil prices remain low. With gold prices high, some CBs are selling to raise cash. Bloomberg also said year-over-year gold supply is down 3%. Meanwhile, CB purchases are forecast to bounce back next year. A second headwind for gold could be volatility. It's possible we might see a strong market selloff if investors panic from an uncertain election outcome. I would expect that to be nothing more than temporary weakness. Still, I see overall strong market winds at gold's back. Support for Higher Gold Legendary investor Stanley Druckenmiller told viewers of the Robin Hood Investors Conference, "We have borrowed so much that I'm skeptical that three to five years out that equities will give us any kind of return." He does however see inflation above 4% and gold prices higher. Meanwhile, the WGC says gold ETFs reached a record high 3,880 tonnes in Q3, acquiring another 272.5 tonnes.

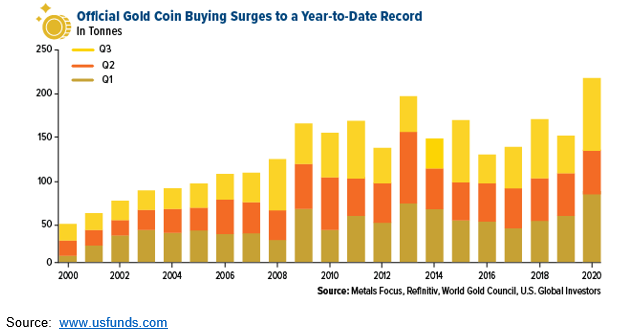

What's more, physical gold buying has just reached an all-time high.

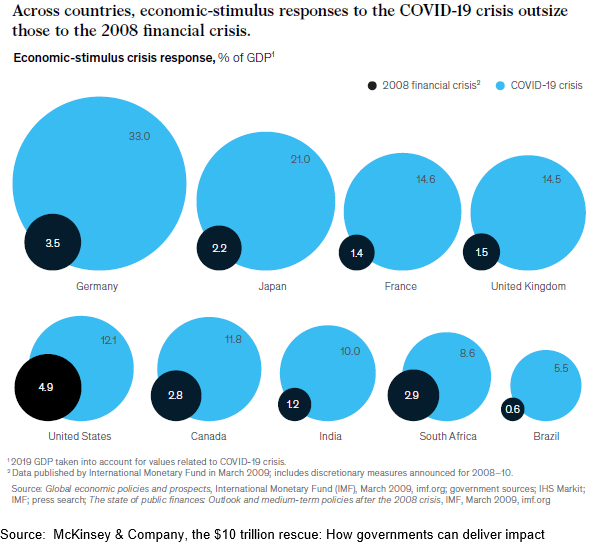

The WGC highlights gold bar and coin buying jumped an astounding 49% year-over-year, reaching 222.1 tonnes through the end of Q3. Don't forget, this is with near-record sustained high gold prices…globally. Much of this is being propelled by low rates and government spending. Trump has proposed a $1 trillion infrastructure plan, while presidential candidate Biden is proposing a $2 trillion green energy and infrastructure plan should he win. That doesn't even account for Covid-19 stimulus spending: a global phenomenon. In June, McKinsey & Company stated, "Governments' economic responses to the crisis is unprecedented, too: $10 trillion announced just in the first two months, which is three times more than the response to the 2008–09 financial crisis.

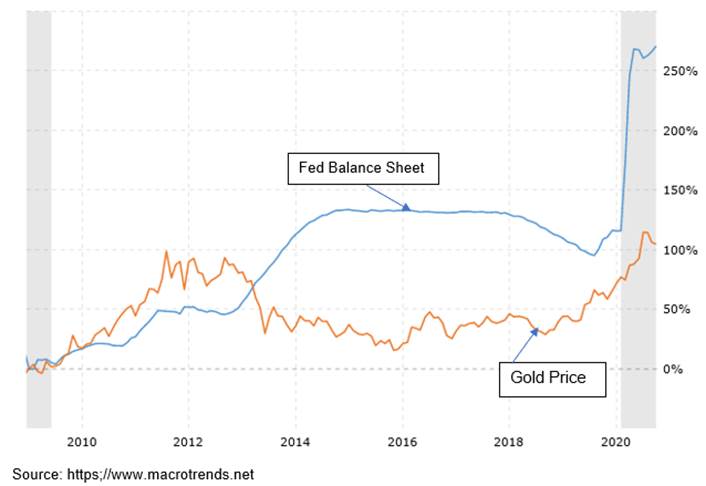

It's not a stretch to conclude that spending, deficits and debt are heading in one direction: higher. Which is why it's easy to see why gold is set to follow. Here's a look at the monthly percentage growth of the Fed's balance sheet versus the gold price (gold in orange, Fed balance sheet in blue).

While this chart is pretty much self-explanatory, I will say that gold has a lot of catching up to do. I'm cautiously optimistic in the near term. But if markets sell off hard, investors will look to raise cash. Be ready for gold and gold stocks to follow, at least initially, as investors sell to meet margin calls. I'd expect a quick recovery though, as wise money steps in on the opportunity to buy the dip. My bottom line is this: A whole lot of promises have been made by both sides in this election. In order to get our votes, politicians try to bribe us with our own money. In the end, you need to ask yourself who really has your greatest interest at heart? I'm most willing to bet on the promise of gold. And I think we'll see a new record high before the year is out. --Peter Krauth Peter Krauth is a former portfolio adviser and a 20-year veteran of the resource market, with special expertise in energy, metals and mining stocks. He has been editor of a widely circulated resource newsletter, and contributed numerous articles to Kitco.com, BNN Bloomberg and the Financial Post. Krauth holds a Master of Business Administration from McGill University and is headquartered in resource-rich Canada. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure:  from https://www.streetwisereports.com/article/2020/11/02/a-golden-election-promise.html Source: Matt Badiali for Streetwise Reports 11/02/2020 Independent financial analyst Matt Badiali homes in on the company's Yukon project."Hey, can you keep watch for me while I fix the Garmin?" I watched uncomfortably as the pilot fiddled with a hand-held GPS in his lap. He looked over at me, briefly. "The cranes are migrating right now, and we really don't want to hit one…" I shifted uncomfortably on the tiny seat. We were a couple thousand feet up somewhere over the Yukon territory. As he looked down at the uncooperative GPS, I went from mildly concerned to acute fear. I spent the rest of the trip gripping the airframe and scanning the skies for giant, plane-wrecking birds. I still don't know if he was kidding. That was back in 2010, in the middle of the last gold bull market. I caught a tiny little plane out of Whitehorse to go up to see Kaminak Gold's Coffee Project. It was my first trip up to the Yukon and I learned a ton about the rich history of the region. Giant gold miner Goldcorp ultimately bought Kaminak for half a billion dollars. Back then, the Yukon was a hot spot. Agnico Eagle, Goldcorp, Newmont and Kinross all invested heavily in the region. So much money went into the ground up there that the New York Times Magazine wrote an article titled "Gold Mania in the Yukon" in May 2011. Just before the wheels came off the gold price. After that, several companies bowed out. Low gold prices and tough working conditions pared the number of companies down to a handful. Fast forward to today and there's another project in the Yukon that I need to go visit, called Klaza. It's one of the few projects that remained active throughout the down years. It's a high-grade gold project run by some great geologists. They worked steadily on this project through the down years. They own it 100% and it has no royalty. Even better, I can drive to it from Whitehorse…no fear of cranes or balky GPS units. The Klaza project sits on the Dawson Gold Belt, just south of Coffee, Casino, Minto, Freegold Mountain and Carmacks Copper. It's less than 50 kilometers by road from the town of Carmacks. The town of Carmack is named for a famous gold explorer. He discovered Bonanza Creek, which kicked off the Klondike Gold Rush. Since 1896, miners took over 20 million ounces of gold out of the sand and placer deposits in the territory. That's why I went to see the area back in 2010. While the prospectors found a lot of gold in sediments, the sources of that gold went relatively unknown. I get excited about that kind of potential. Because it means that some smart, enterprising geologists could still strike it rich. And make no mistake, I want to go see this one. It looks attractive on paper, for sure. The company just issued a preliminary economic assessment in 2020. The average grade of its indicated resource is 4.8 grams per ton gold and 98 grams per ton silver. The net present value (at $1,740 per ounce gold) comes in at C$540 million—more than fifteen times the current market cap. That kind of multiple means I'm interested. The reason the opportunity exists is because it's a bunch of geologists working on a real gold deposit…but no loud-mouthed promoter hawking it to the unsuspecting public. It's just sitting there, under the radar. Every time the gold price goes up, it gets a little bit richer. The company still has a lot of work to do. Only three of eleven known zones are in the resource estimate. And there's still room to find more gold. They haven't hit the end of the mineralized rock yet. And they have more prospecting to do nearby. So, if you are looking for a gold deposit that hasn't moved with the gold price yet, check out Rockhaven Resources Ltd. (RK:TSX.V). It is a C$31 million junior in the Yukon's historical Dawson Gold Belt, sitting on a great looking gold deposit. --Matt Badiali Matt Badiali is a geologist and independent financial analyst. He spent fifteen years researching and writing about great investments inside the natural resources sectors. He can be reached at www.mattbadiali.net. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsStreetwise Reports Disclosure:

( Companies Mentioned: RK:TSX.V, ) from https://www.streetwisereports.com/article/2020/11/02/rockhaven-resources-an-overlooked-yukon-junior-with-a-big-discovery.html Source: Streetwise Reports 11/02/2020 The highlights of the Nomad Royalty Company story are delivered in a Haywood report.In an Oct. 15 research note, analyst Kerry Smith reported that Haywood initiated coverage on a recent entrant to the royalty/streaming space, Nomad Royalty Company Ltd. (NSR:TSX; NSRXF:OTCQX), with a Buy rating and a CA$2.25 per share 12-month target price. Nomad's stock is trading now at about CA$1.24 per share, at a discount to its peers, Smith noted. "Given Nomad's growth profile, ability to source accretive deals, strong shareholder base and access to capital, we expect this discount to close over time as Nomad attains critical mass," added Smith. Nomad is "starting out with a bang and wasting no time," the analyst wrote. The analyst recapped what the Quebec-based company has accomplished in a short period of time. Since its founding in February 2020 by a trio of former Osisko Royalties employees with vast experience in the space, Nomad already has purchased eight royalties and streams, one gold loan and one commercial production payment. Subsequently, after going public in May 2020, it made three additional royalty transactions. "Nomad's strategy is to acquire advanced stage or producing royalties and use their shares as primary consideration, allowing vendors to participate in the upside over time as Nomad's valuation increases," explained Smith. Further, the company already started paying out a $0.02 per share annual dividend, paid quarterly; it made its first payment on Oct. 15, 2020. To maintain this dividend, Nomad is striving to get its general and administrative expense down to be the lowest in the sector. Smith presented Nomad's other attractive elements. For one, the company has a "healthy mix" of both production- and development-stage assets, assuring it cash flow now and in the future. Of Nomad's 11 assets, which are located in Australia, Africa and North America, six are producing (Bonikro, Mercedes, RDM, South Arturo, Gualcamayo and Moss). From those, Nomad generated about US$13 million in Q2/20, achieving a cash flow margin of about 89%. One asset is on care and maintenance (Woodlawn), another is slated to commence production in late 2020-early 2021 (Blyvoor) and a third is in development (Robertson). Also, Smith relayed, Nomad has "partners with deep pockets," specifically Orion Mine Finance, which owns 75.6% of Nomad's shares, and Yamana, which owns 12.7%. These companies "provide support for Nomad through both equity ownership positions and collaboration on royalty acquisitions that should help it continue to grow and remain competitive against its peers in royalty transactions," Smith indicated. As for the outlook for Nomad, Smith commented that it "has primary exposure to both silver and gold, two commodities which we believe are now in a bull market, and the company is positioned to grow revenue, cash flow and dividends over time." Read what other experts are saying about: Disclosure: Disclosures from Haywood Securities, Nomad Royalty Company Ltd., October 15, 2020 Analyst Certification: I, Kerry Smith, hereby certify that the views expressed in this report (which includes the rating assigned to the issuer’s shares as well as the analytical substance and tone of the report) accurately reflect my/our personal views about the subject securities and the issuer. No part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendations. Important Disclosures Research policy is available here.

( Companies Mentioned: NSR:TSX; NSRXF:OTCQX, ) from https://www.streetwisereports.com/article/2020/11/02/coverage-initiated-on-royalty-firm-starting-out-with-a-bang-and-wasting-no-time.html Alianza Minerals Closes Oversubscribed Financing at C$3.2M Drilling at Haldane Has Commenced10/31/2020 Source: The Critical Investor for Streetwise Reports 10/30/2020 The Critical Investor profiles this silver-focused explorer with three projects, two in the Yukon and one in Nevada.All pictures are company material, unless stated otherwise. All currencies are in US Dollars, unless stated otherwise. As I discussed recently in other articles, 2020 is shaping up to be a remarkable year, with COVID-19 disrupting the markets and real economy, prompting central banks around the world with huge stimulus packages to perform damage control. The negative real interest rates combined with a devaluating U.S. dollar appeared to be the perfect storm for precious metals, including silver, the metal of focus for Alianza Minerals Ltd. (ANZ:TSX.V). This Kitco chart shows the explosive extent of this year's run up of the gray metal, after years of flatlining:

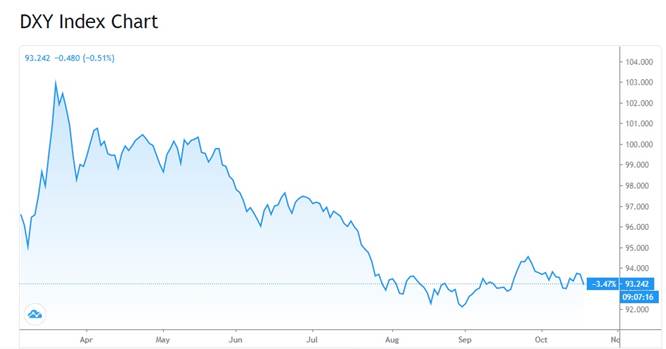

Silver has been correcting lately as the U.S. dollar is regaining some strength on the premise of being a safe haven lately, on the background of encouraging economic data, the second COVID-19 wave, fears linked to trade war tensions with China and, last but not least, the upcoming presidential elections in the U.S. Analysts overall expect the latest surge of the U.S. dollar not to last very long, as the Fed's dovish policies are likely to continue, and are negative for the yield advantage of dollar-denominated assets. The short recovery in September can be seen here in this chart of Tradingview:

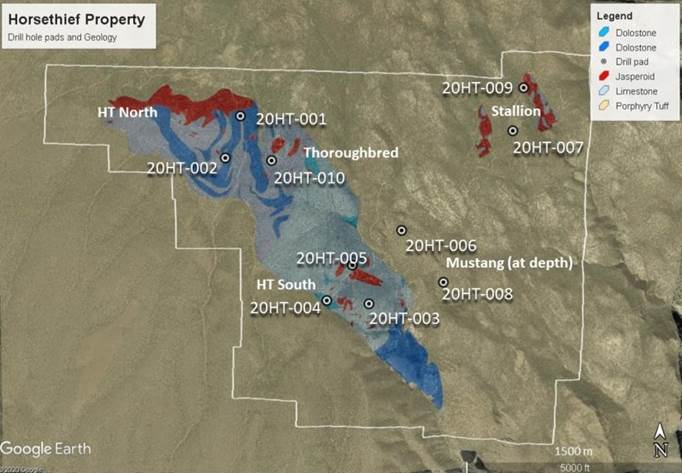

A low U.S. dollar price is usually a positive for precious metal prices, especially in combination with a negative real interest environment as we have now, and which seems to be forecasted for several years from now, as the colossal U.S. debt will have problems handling any serious increase in interest rates. In the meantime, Alianza Minerals has been busy this summer and autumn after the COVID-19 lockdown was lifted, with a variety of activities. After having received the BLM approval for more drilling at its Horsethief project in Nevada, most of the second quarter was filled with reverse circulation (RC) drilling by JV partner Hochschild.

The first three holes didn't intercept significant mineralization, but anomalous gold like 12.2m @ 0.13g/t Au and 19.9m @ 0.11g/t in best hole 20HT-003. The next three holes returned nothing special either, with one hole reporting noteworthy anomalous values, being 3m @0.141g/t Au for hole 20HT-005. CEO Jason Weber is still positive: "The first six holes at Horsethief have demonstrated the presence of alteration and mineralization features typical of productive gold mineralizing systems over a broad area," stated Jason Weber, President and CEO of Alianza Minerals. "We are encouraged by the size of the mineralizing system and confirmation of gold mineralization in carbonates beneath younger volcanic cover but have only intersected anomalous gold values to date. The four remaining holes all tested further, under-evaluated parts of the system particularly at the Stallion and Thoroughbred targets." At first sight the results seem disappointing, as they didn't even come near the historical drill results from the 1980s:

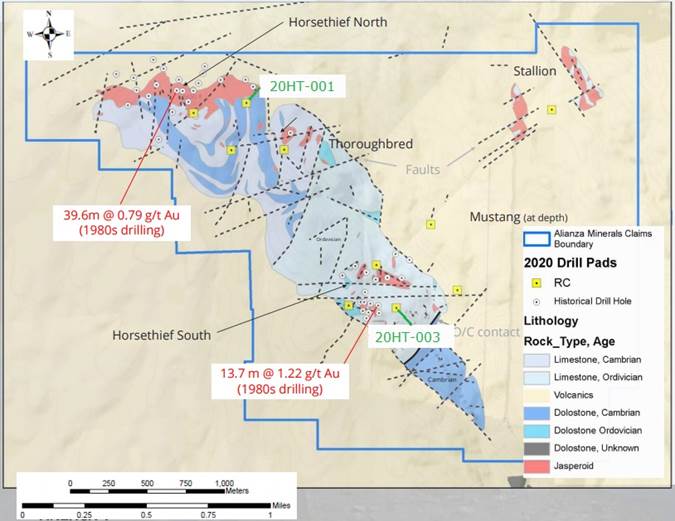

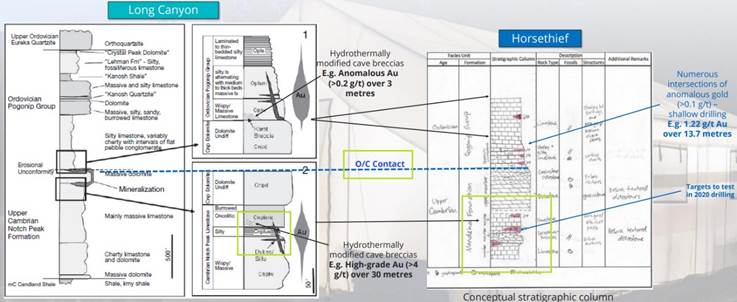

Hole 20HT-003 was only about 100 meters from the historical hole that reported 13.7m @ 1.22g/t Au. It appears that the area is faulted a lot (the dotted lines are fault lines), which could complicate the finding of the structural controls. Alianza is looking to find another Long Canyon as it has similar geological characteristics. Both projects have a contact between Ordovician quartzite and Cambrian limestone/dolomite, the so-called O/C Contact. In line with this, the low grade intercepts were also found at Long Canyon in breccia layers, just like with Horsethief so far. Alianza was also looking to test the deeper targets in this campaign, following the Long Canyon analogy:

Holes 20HT-006, 007 and 008 were targeting this contact beneath volcanic rocks that were hypothesized to cover the prospective stratigraphy, and this was proven correct according to management, interpreting the results of the final four holes that have been reported on October 22. Unfortunately, regarding intercepts, only hole HT20-009 hit a very modest 76m intersection of anomalous gold results up to 0.185g/t, the other three didn't return results worth mentioning. This is obviously disappointing, although many indicators point towards the right direction. CEO Jason Weber had also hopes for more, but was honest about the results so far, as he showed in the news release: "Although clearly not the discovery we were hoping for, the size and distribution of altered carbonate rocks along with widespread anomalous gold concentrations is encouraging. We will carry out a detailed examination of the pathfinder elements from the ICP data once it is available from the lab to determine if any vectors towards remaining targets exist." After discussing the results a bit more in-depth with him, I asked him what he needs to find in the data in order to remain on track with the O/C Contact Long Canyon concept, if he thinks he has to adjust his strategy for this, or what kind of alternative concept he thinks could be present as well. Furthermore I wondered if Hochschild is only interested in the Long Canyon type opportunity, or is also open to investigate further. Weber had this to say: "While the gold results have been disappointing, we don't have the multi-element ICP results for most of hole four and holes five to ten. Hopefully this data will help vector to more productive portions of the system. Any decisions on how to proceed will be made after examining that data." In between reporting the first and second batches of Horsethief results, the company also announced the hiring of a VP Exploration Rob Duncan, a very experienced geologist (Rio Tinto, Inmet) and a pretty solid addition to management. Weber was pretty happy with the hiring of Duncan: "Besides being an excellent technical mind, Rob allows Alianza to be active on more projects, including generating the next set of exploration targets to be optioned out." At the end of the Horsethief drill program, Alianza also acquired the lease of the Twin Canyon Gold prospect in southwestern Colorado, for up to C$200k in cash and up to 2 million shares in 10 years, depending on the achievement of several milestones. The claims are organized around a small underground gold mine that operated at Twin Canyon during the 1980s and early 1990s. Historical sampling of the underground workings has returned grab samples ranging from 0.1 to 15.77 g/t gold. Twenty-eight historical channel samples 1.5 to 10 meters in length were anomalous in gold, eight of which exceeded 2 g/t gold (highlight of 8.1 g/t gold over 3 meters). Historical rotary drilling confirms the presence of a gold grade over 0.5 g/t over a 500 by 500 meter area, indicating disseminated gold mineralization with low and high grade areas. The company completed a first soil sampling program, and based on this it has commenced a second exploration program, which will consist of detailed prospecting and geological mapping within areas of gold soil anomalies, expansion of the first soil sampling campaign, and detailed structural mapping to determine the primary controls focusing on gold mineralization. All this exploration work has to be funded of course, and the company has been busy on that front as well, culminating in the close of an oversubscribed C$3.2 million financing on October 16, 2020. This round consisted of C$1 million non-flow through at C$0.135 and a 2 year 20c half warrant, and C$2.2 million flow through, at C$0.155 and no warrants. The non-flow through proceeds will be spent on Nevada and Colorado exploration and working capital, the flow through proceeds will be spent on Yukon exploration, including Haldane. As the company is cashed up nicely now, investors are waiting in anticipation for incoming results, the share price obviously being supported by higher silver prices:

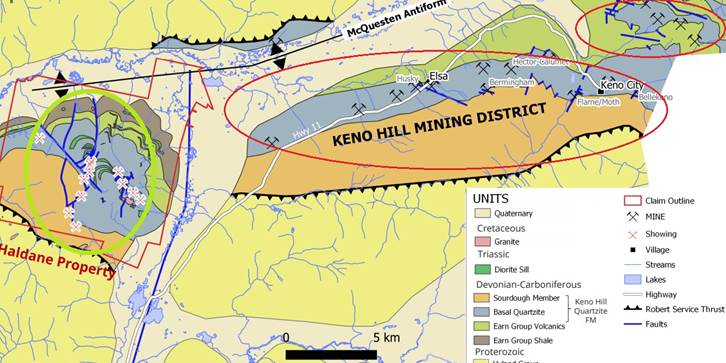

As the company has several ongoing exploration projects, and Horsethief wasn't its flagship project (which is Haldane), the share price has held up relatively well after the disappointing news of Horsethief, but is now suffering like almost all juniors from election risks in the markets. Closing the oversubscribed financing slightly above the current levels didn't hurt either. Investors are clearly curious what Alianza could achieve here. Besides Haldane and Horsethief, another exploration project is the Tim Silver project in the Yukon, part of a JV with Coeur Mining. Exploration at Tim is targeting high-grade silver-lead mineralization similar to that being mined by Coeur at its Silvertip operation, located 12 kilometers south of the property. As the new owner of Silvertip, which has a relatively limited resource and likewise mine life, Coeur could have an interest in Tim to develop it as a backup resource, if Silvertip exploration doesn't generate the desired resource expansion. If Tim results in an economic resource, it could at the very least serve as an extra source of ore for the Silvertip mill and processing plant. Of course the hypothetical Tim resource would need to have the same metallurgy otherwise Coeur would have to install a different flow sheet at the processing plant, increasing sustaining capex further. According to Weber, the potential for likewise metallurgy is one of the reasons Coeur is keen on Tim, as it sees the same units and style of mineralization so it feels the metallurgy has a good chance to likely be similar. The exploration program at Tim is expected to target high-grade silver-lead-zinc Carbonate Replacement Mineralization ("CRM"), similar to that found at Coeur's Silvertip operation. Coeur's exploration plans will consist of detailed mapping, soil geochemical surveys and reopening old trenches. Coeur has been very active with a multi-rig drilling program at the Silvertip Mine and surrounding exploration targets this summer, and its work will be looking for analogies between the geology at Tim and the Silvertip Mine. Currently, the status and results of this exploration program for Tim is as follows, according to CEO Weber: "Coeur has pushed back the exploration program at Tim to early 2021, to allow for the remediation of the access into the property. The idea is to identify targets for a larger program to take place later in 2021." So Alianza has to wait longer than anticipated for Tim Silver exploration, but fortunately it still has its flagship Haldane Silver project with a drill rig turning now. Until recently, the Haldane Silver project in the historical Keno Hill Mining District in the Yukon has seen the most reconnaissance exploration work, although not too much drilling. According to Weber, this could imply promising exploration potential at several targets at both the Middlecoff Zone and West Fault. Alianza is looking to find economic concentrations of vein type mineralization in the Keno Hill District, similar to the numerous historical mines, as can be seen on this map (red ellipses represent mines, green represent silver showings, both located within the gray Basal quartzite units):

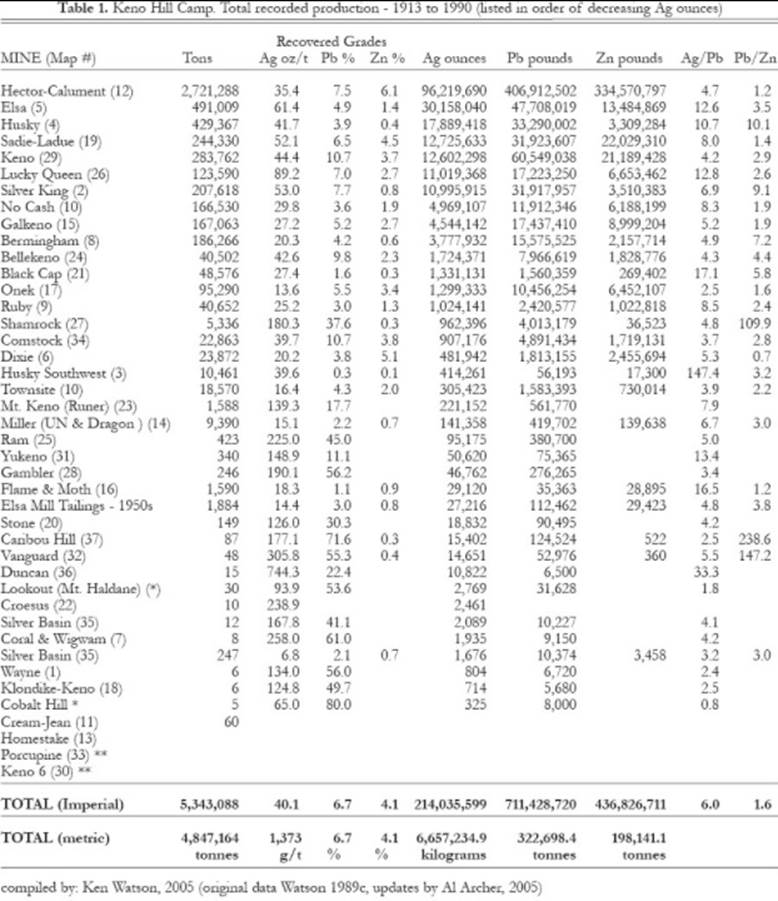

To get an impression of silver, zinc and lead production of the Keno Hill mining district, management was so kind to provide me with a table containing production of all separate mines:

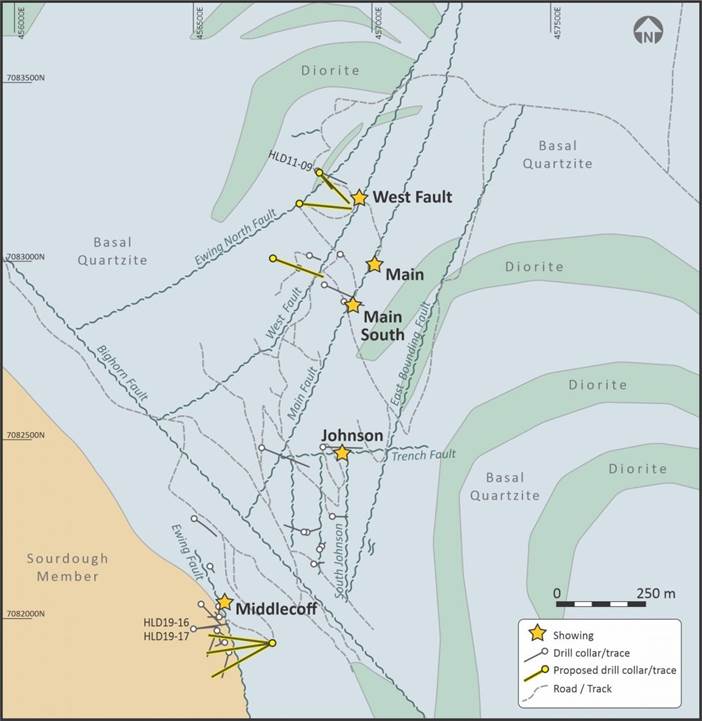

Quite a few mines exceeded 10 Moz Ag, and producing, for example, 1 Moz Ag per annum at grades over 30 oz/t should generate very profitable mines nowadays, so it is clear for me where Alianza is after. Historical drill results at Haldane generated 2.2m @ 320g/t Ag, 1.1g/t Au and 0.7% Pb at West Fault, and drilling in 2019 returned 1m @455g/t Ag and 0.35m @ 996g/t Ag, 1.486g/t Au and 28.35% Pb in hole HLD19-16 at Middlecoff Zone. Another historical underground hole returned 1.2m @ 2,791g/t Ag.

The phase 1 drilling program has commenced on October 26, a phase 2 program is planned for the spring of 2021, which will also target the recently discovered Bighorn Zone (2.35m@125g/t Ag, 4.39% Pb). The yellow marked collars represent the proposed trajectories of the current program:

I wondered about the analogies between Haldane and the other deposits in the Keno District, and why management thinks the historically mined, silver-rich mineralization is likely to continue at Haldane. Did they identify deeper feeder systems that could have provided silver to all these quartzite zones? Weber had this to say: "It is clear that the mineralization at Haldane shares all the key characteristics that define Keno-style mineralization: vein and breccia mineralization which is hosted in structurally controlled, complex vein systems with northerly orientations located in proximity to the Robert Service Thrust Fault on the south limb of the McQuesten Anticline within the prospective Basal quartzite unit. "Additionally, Haldane vein mineralization is comprised of the same mineralogy, galena, sphalerite, tetrahedrite and likely pyrargyrite in manganiferous carbonate and quartz veins. Historical mining at the Middlecoff and Johnson zones at Haldane was very limited in scope and our work in 2019 at Middlecoff points to a high-grade shoot that is relatively flat in its orientation. With high-grade silver mineralization almost 150 meters to the south in the 1960s underground hole UM-02, we feel there is excellent potential for the Middlecoff zone to extend to the south, that we can test in this program." Looking at the maps, it seems logical for the mineralized quartzite to continue, but as we all know exploration nearology isn't that simple. Let's wait and see what the drill bit brings in. Conclusion With the recent closing of an oversubscribed financing of C$3.2 million, Alianza Minerals has a full treasury, and is able to continue drilling at Haldane now, start at Tim next year and, if warranted, could continue at Horsethief. The drilling results at Horsethief disappointed so far, but management and Hochschild aren't ready to call it a day here, and further analysis of drilling data could be putting the pieces of a difficult puzzle together after all. Greenfield exploration is not easy, and a nice example of this that I often use is the famous "Hole 76," indicating that the legendary Hemlo deposit was found only after drilling 75 holes with no results. Times have changed of course, and investors aren't as patient anymore as they were back then, with less options to their disposal at the time and no 24/7 information compared to these days. Notwithstanding this, Alianza is working diligently at three exploration assets, and in my view at least two chances at success. Let's see what Haldane drilling could have in store for us first.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published. The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsCritical Investor Disclaimer: Streetwise Reports Disclosure: Charts and graphics provided by the author.

( Companies Mentioned: ANZ:TSX.V, ) from https://www.streetwisereports.com/article/2020/10/30/alianza-minerals-closes-oversubscribed-financing-at-c-3-2m-drilling-at-haldane-has-commenced.html Source: Streetwise Reports 10/30/2020 The reasons why Nomad Royalty Co. makes an attractive investment are presented in a Scotiabank report.In an Oct. 21 research note, analyst Trevor Turnbull reported that Scotiabank initiated coverage on Nomad Royalty Company Ltd. (NSR:TSX;NSRXF:OTCQX) with a Sector Outperform rating "because of its best-in-class cash flow and production growth." Scotiabank's one-year target price on the company is CA$2 per share, which compares to about CA$1.23 per share currently. Turnbull provided his investment thesis for this newly formed royalty and streaming company. Montreal-headquartered Nomad owns five precious metal streams, four gold royalties and one gold loan. Its assets are located in eight jurisdictions in Australia, Africa and North America. With its business model, the mining company offers investors leverage to rising bullion prices without the costs and risks associated with building and operating mines, the analyst noted. The company also offers upside from increases to production, mine lives, resources and exploration without having to make additional investments. Nomad pays a quarterly dividend of CA$0.02 per share. With 74%, or eight, of its assets expected to generate cash flow in 2020, Nomad has more active projects than three of its peers, Maverix, Osisko and Sandstorm. Of this group, Nomad has the highest projected 2020–2023 cash flow and production CAGR, of 31% and 29%, respectively. "We have a high degree of confidence in these numbers and our valuation," Turnbull commented. He highlighted that Nomad's projected production growth through 2023 and beyond "stands out," and will result from the ramp-up of existing assets and further royalty/streaming acquisitions. For example, the Blyvoor mine in South Africa is scheduled to pour gold by year-end and ramp up in 2021. The Woodlawn mine in Australia is expected to increase production in 2022. The Robertson property in Nevada is anticipated to start generating cash flow in 2027. Nomad is well positioned financially to make more deals as it has a growing cash balance, available liquidity and no debt. "We estimate that the company is able to deploy approximately $100 million from cash and up to a $75 million revolving line of credit," noted Turnbull. Scotiabank estimates Nomad will have $25 million in cash at the end of this year. Another positive to the Nomad story is that its three co-founders and executives, Vincent Metcalfe (CEO), Joseph de la Plante (chief investment officer) and Elif Levesque (chief financial officer), previously worked together, in the royalty/streaming space, for many years. "We believe this is a valuable benefit that greatly reduces the learning curve," Turnbull wrote. As for Nomad's stock, corporate partners Orion Mine Finance and Yamana Gold, along with Nomad management and directors, own about 90% of it. Looking forward, Turnbull indicated that upcoming catalysts for Nomad include production announcements, such as Blyvoor's first gold by year-end 2020; development milestones, including the finalization of the Woodlawn strategic process and subsequent restart plans; and asset derisking, namely completion of technical reports and detailed mine plans for Blyvoor, Bonikro and Woodlawn. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure: Disclosures from Scotiabank, Nomad Royalty Company Ltd., October 21, 2020 The Research Analyst(s) responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting market information. I, Trevor Turnbull, certify that (1) the views expressed in this report in connection with securities or issuers that I analyze accurately reflect my personal views and (2) no part of my compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed by me in this report. Research Analyst compensation is not based on investment or corporate banking revenues; however, compensation may relate to the revenues of Scotiabank as a whole, of which investment banking, corporate banking, sales and trading are a part.

( Companies Mentioned: NSR:TSX; NSRXF:OTCQX, ) from https://www.streetwisereports.com/article/2020/10/30/coverage-initiated-on-new-royalty-and-streaming-hunter-with-best-in-class-cash-flow-and-production-growth.html Source: Streetwise Reports 10/29/2020 Shares of Alamos Gold traded 12% higher after the company reported record free cash flow in Q3/20 and a 49% sequential increase in gold production versus the previous quarter.Intermediate gold producer Alamos Gold Inc. (AGI:TSX; AGI:NYSE) yesterday announced financial results for its third quarter of 2020 ended September 30, 2020. The company's President and CEO John A. McCluskey commented, "We had an excellent third quarter financially and operationally with strong performances at all three operations driving costs significantly lower. This included another record quarter at Island Gold and Young-Davidson starting to demonstrate its full potential following the completion of the lower mine expansion. We previously outlined our expectation to transition to strong free cash flow generation in the second half of 2020 and we delivered with record free cash flow of $76 million in the quarter." "Given our strong free cash flow outlook, we are pleased to announce a 33% increase in our dividend, which has now grown by 300% since 2018. We expect to continue to generate strong free cash flow while reinvesting in high-return projects like La Yaqui Grande and the Phase III Expansion at Island Gold which will support further growth and returns to shareholders," McCluskey added. The company reported on several operating and financial highlights and stated that it achieved record quarterly free cash flow of $76.0 million in Q3/20 driven by higher margins at all of its operations. The firm indicated that it produced 117 Koz Au in Q3/20, which was a 49% increase compared to Q2/20. Alamos Gold commented that the increase was due to production returning to budgeted levels following the temporary suspension of operations due to COVID-19 at the Island Gold and Mulatos mines in Q2/20. The company pointed out that through the first nine months of the 2020 fiscal year it has produced 306.4 Koz gold and remains very well positioned to meet its FY/20 guidance of 405-435 Koz gold. Alamos stated that in Q3/20 it sold 116.035 Koz Au at an average price of $1,882/oz, resulting in revenues of $218.4 million. The firm additionally announced that it was increasing its common shareholder's dividend by 33% to US$0.08 per share starting with the dividend payable in December 2020. The company stated that the increase is justified and supported by the record free cash flow in Q3/20 and strong forward outlook. The company noted that in Q3/20 consolidated total cash costs were $681 per ounce and all-in sustaining costs were of $949 per ounce and that both of these decreased significantly from H1/20. Alamos reported that it reported record adjusted net earnings of $56.9 million, or $0.15 per share in Q3/20, which increased by 143% compared to Q3/19. The firm additionally reported that in the quarter it realized record net earnings of $67.9 million, or $0.17 per share. The company indicated that the record financial performance it achieved in Q3/20 was due to a combination of very strong operational performance and higher gold prices. The firm advised that gold production increased to 117.1 Koz in the quarter, which represented a 49% increase over Q2/20. The company added that these volumes were registered along with much lower total cash costs of $681 per ounce. Alamos Gold advised that it expects that production in Q4/20 will be at similar levels, which will position the company to meet its revised FY/20 production and cost guidance that the firm issued earlier this year in July. Alamos Gold is an intermediate gold producer headquartered in Toronto. The company employs more than 1,700 people and operates three mines in North America, which include the Island Gold and Young-Davidson mines in northern Ontario and the Mulatos mine located in the state of Sonora in Mexico. The firm noted that it also has a large number of other development stage projects in the U.S. Turkey, Canada and Mexico. Alamos Gold started the day with a market capitalization of about $3.2 billion with approximately 391.4 million shares outstanding. AGI shares opened 3% higher today at US$8.36 (+$0.24, +2.96%) over yesterday's US$8.12 closing price. The stock has traded today between US$8.32 and US$9.19 per share and is presently trading at US$9.11 (+US$0.98, +12.05%). Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure:

( Companies Mentioned: AGI:TSX; AGI:NYSE, ) from https://www.streetwisereports.com/article/2020/10/29/alamos-gold-posts-record-cash-flow-in-q3-confirms-fy-guidance-and-raises-dividend-33.html |

RSS Feed

RSS Feed