|

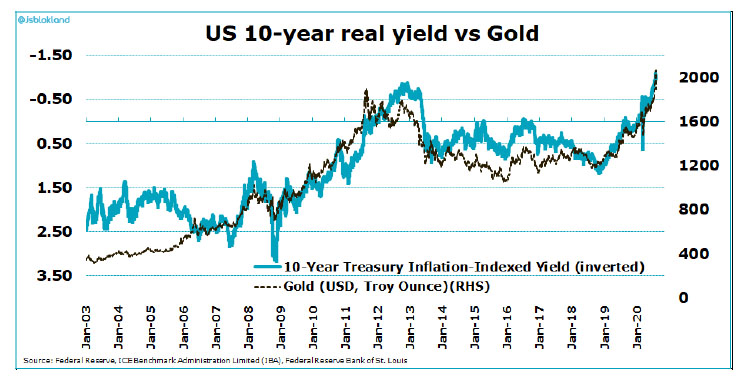

Source: Rudi Fronk and Jim Anthony for Streetwise Reports 11/12/2020 Rudi Fronk and Jim Anthony, cofounders of Seabridge Gold, look at the macroeconomic factors they believe will move gold higher.The gold market entered a period of increased volatility during the third quarter, usually a positive indicator for the metal. A growing number of investors and analysts recommended the accumulation of gold as it began to move out of the shadows and into the spotlight. Global ETFs have now been net purchasers for 11 months in a row and central banks have also been net purchasers every month of this year except October when two nations liquidated some of their holdings to meet dollar requirements resulting from the COVID-induced economic crisis. We see a further move higher in gold in the near term as the election log jam begins to clear. The election process curtailed new fiscal stimulus since July when direct transfers to individuals exhausted their Congressional approvals. This pause in fiscal stimulus, which took government transfer payments to an astonishing 25% of household income, coincided with a pause in gold's upward momentum. However, it is very clear that further stimulus is favored on both sides of the House and even a Republican Senate, if there proves to be one, will not prevent trillions more of fiscal stimulus. The two main drivers of the gold price are the dollar and real yields. We expect both drivers to be positive in the coming year. First, the dollar: The Fed will be forced to fund whatever expenditures the Congress approves. Foreign holdings are at 10-year lows as the largest sovereign purchasers became net sellers this year. We therefore expect Fed debt monetization to accelerate in the next few months with a negative impact on the dollar. It was a $3 Trillion expansion of the Fed balance sheet in March and April which, not coincidentally, equaled a sudden increase in the US deficit to $3 Trillion, that unleashed gold from its March low. Debt monetization is a formula for dollar weakness. As for yields, the market narrative now favors a reflation trade due to the apparent success of the US Operation Warp Speed vaccine initiative. This has provoked the sale of Treasuries as hot money has moved back into stocks, driving up yields. We expect the Fed response to be aggressive: higher yields cannot be allowed to dampen the economic recovery. In our view, the Fed is very likely to cap yields, a policy that can only be implemented by more QE. Capping yields in unison with a reflation narrative means increased inflation expectations and lower real yields…the magic formula for higher gold prices. If yields cannot rise to attract and hold private capital, the Fed must buy more debt and the dollar must fall. Remember that today's QE is not the QE post Great Recession which corralled the new money in the financial system, resulting in a muted response in terms of money supply growth and inflation. Today's QE is being mainlined into the real economy by way of direct transfer payments to individuals and business, forgivable loans and bailouts. Money supply is expanding at a blistering pace. The die has been cast and there is no turning back. Going forward, gold is the best protection for private wealth and there is not nearly enough of it to serve this purpose at current prices.

In a reflation scenario, inflation expectations rise significantly from low levels. With the rise in nominal yields capped by central bank QE, real yields fall. The relationship between real yields and gold is virtually perfect in recent years.

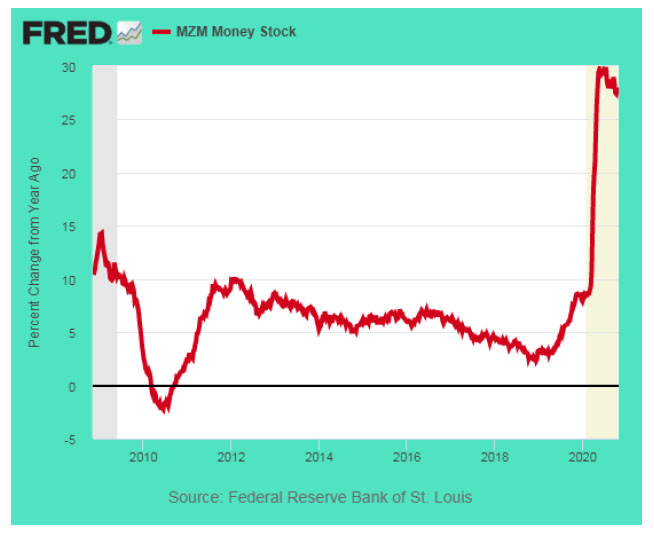

The growth in MZM money supply...the money available for immediate expenditure...has slowed(!) to 27.5% year over year, down from 30% two months ago, an unprecedented pace of money creation which is temporarily keeping the economy afloat. This article is the collaboration of Rudi Fronk and Jim Anthony, cofounders of Seabridge Gold, and reflects the thinking that has helped make them successful gold investors. Rudi is the current Chairman and CEO of Seabridge and Jim is one of its largest shareholders. Disclaimer: The authors are not registered or accredited as investment advisors. Information contained herein has been obtained from sources believed reliable but is not necessarily complete and accuracy is not guaranteed. Any securities mentioned on this site are not to be construed as investment or trading recommendations specifically for you. You must consult your own advisor for investment or trading advice. This article is for informational purposes only. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosures:  from https://www.streetwisereports.com/article/2020/11/12/whats-ahead-for-the-gold-market.html

0 Comments

Source: Streetwise Reports 11/12/2020 Shares of SSR Mining traded 10% higher after the company reported Q3/20 earnings and stated that it was on track with its full-year guidance to produce 680-760 Koz gold equivalent in FY/20.SSR Mining Inc. (SSRM:NASDAQ) today announced third quarter operating and consolidated financial results for the period ended September 30, 2020. The company's President and CEO Rod Antal commented, "With the transformational merger with Alacer Gold finalized, integration efforts near completion, and our operations running at steady state following COVID-19 interruptions, the focus has turned towards delivering a number of value enhancing catalysts before year-end." "We anticipate a robust fourth quarter with strong free cash flow generation, further strengthening our balance sheet. This continued peer-leading free cash flow generation has allowed us to put in place a dividend policy beginning in the first quarter of 2021...A recurring quarterly dividend is expected to be the primary method of capital return, and we will periodically evaluate supplementing this dividend from trailing excess attributable free cash flow through incremental dividends and/or share buyback programs, Antal added." The firm reported that in Q3/20 it produced a total of 106.84 Koz gold equivalent (Au eq)and sold 115.31 Koz Au eq in the same period. These amounts compared favorably to the 104.78 Koz Au eq produced and 95.11 Koz Au eq sold in Q3/19. SSR Mining reported that on a consolidated basis it posted total revenues of $225.4 million in Q3/20, compared to $147.9 million in Q3/19. During the period the firm indicated that net income attributable to equity holders of SSR Mining was $26.75 million, or $0.19 per share, versus $20.74 million, or $0.17 per share in the prior year's corresponding quarter. The firm advised that on a non-GAAP basis it posted adjusted attributable net income of $67.8 million or $0.49 per share in Q3/20, compared to $35.78 million, or $0.29 per share in Q3/19. The company touched on several of the operating highlights in the latest quarter and noted that it closed the zero-premium merger with Alacer and that in doing so created a leading intermediate precious metals producer with an experienced leadership team, robust margins and strong free cash flow. The firm additionally announced that its Board of Directors approved the issuance of a quarterly cash dividend in the amount of $0.05 per share beginning in Q1/21. The company advised that it remains on track to meet its FY/20 updated production guidance and stated that production year-to-date has been 491.821 Koz Au eq across the company's four operations. Factoring in the completion of the merger with Alacer, the company stated that its FY/20 outlook estimates production of 680-760 Koz Au eq with all-in sustaining costs (AISC) of $965-1,040 per oz Au eq. SSR Mining Inc. is an intermediate gold company with four producing assets located in Argentina, Canada, Turkey and the U.S., which in 2019 produced in aggregate greater that 720 Koz gold and 7.7 Moz silver. The firm also is actively involved in many other high-quality development and exploration assets in Canada, Mexico, Peru, Turkey and the U.S. SSR Mining has a market capitalization of around $4.0 billion with approximately 219.2 million shares outstanding and a short interest of about 2.25%. SSRM shares opened 5.5% higher today at $19.12 (+$1.00, +5.52%) over yesterday's $18.12 closing price. The stock has traded today between $18.46 and $20.09 per share and is currently trading at $19.84 (+$1.72, +9.49%). Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure:

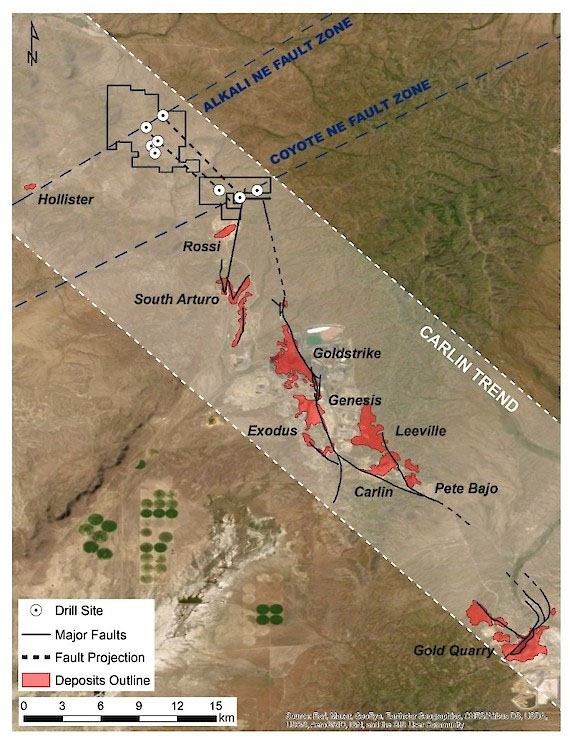

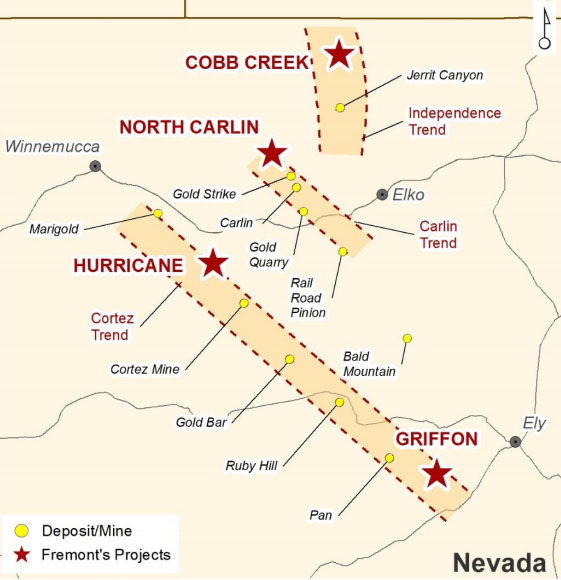

( Companies Mentioned: SSRM:NASDAQ, ) from https://www.streetwisereports.com/article/2020/11/12/ssr-mining-shares-trade-higher-on-q3-earnings-and-approved-dividend-policy.html Source: Streetwise Reports 11/12/2020 With four gold projects in Nevada, Fremont Gold looks to make a new gold discovery in the state.Nevada's Carlin Trend is a behemoth, having produced more than 84 million ounces of gold since the 1960s. To get an idea of what is still in the ground, the Carlin Complex, operated by Nevada Gold Mines, the Barrick Gold and Newmont joint venture, sports a resource of 30 million ounces gold in the Measured and Indicated category. Fremont Gold Ltd. (FRE:TSX.V; FRERF:OTCQB; FR2:FSE) aims to add to the Carlin Trend gold tally through exploration on its 100%-owned North Carlin project. North Carlin is surrounded by some high-grade neighbors. It is 6 kilometers from Nevada Gold Mines and Premier Gold Mines' South Arturo mine, where recent drilling returned 39.6 meters of 17.11 grams per tonne (g/t) gold, 12 kilometers from the Goldstrike Mine, operated by Nevada Gold Mines, which hosts 11.1 million ounces of gold in the Measured and Indicated category, and Hecla Mining Company's Hollister Mine lies just 6 kilometers west.

The North Carlin project is large—more than 42 square kilometers—and largely underexplored. That is about to change because Fremont just announced a drill program there. "Permitting is well underway at North Carlin and drilling should be underway later this month. We are excited to get started as we have developed a number of untested drill targets," Fremont CEO Blaine Monaghan said. "North Carlin is situated in the right geological setting for the discovery of a major gold deposit," Monaghan added. "Fremont has developed several drill targets based on soil geochemistry, gravity and geomagnetic surveys, and the projection of key faults that control gold mineralization in the Carlin Trend." Fremont is permitting 10 drill sites and plans to begin with three holes of up to 500 meters each. "We are starting off with a relatively small first phase drill program of three holes and may add an additional hole or two. We hope to complete the drill program by mid-December but we are prepared to drill it into the winter months," Monaghan stated. With the backlog at the labs this season as a result of COVID restrictions along with increased exploration, Fremont expects to receive assays in February or March, depending on when the drilling ends. Fremont also plans to begin exploration work on its Cobb Creek project, situated in Nevada's Independence Trend, that it has optioned from Contact Gold. Cobb Creek hosts a historical resource of 54,864 ounces of gold in oxides and 118,134 ounces of gold in sulphides, but the property has not been drilled in almost 30 years. "We want to get in there this spring; it hosts that historical resource, but the resource is hosted in a different deposit style," Monaghan said. "We think it has good potential for a Carlin-type deposit. We want to do some early-stage exploration work, using the Carlin model to identify what targets we think have the best potential for a Carlin-type discovery, and then start the permitting process."

Earlier this year, Fremont drilled a nine-hole program at its Griffon project, also in Nevada, in the Cortez Trend. "While the first three holes returned pretty good results, such as 50.3 meters of 1.05 gram per tonne gold starting near surface, we weren't able to return another interval that looked like that in the remainder of the holes," Monaghan said. "We're interpreting all of the new data to help us vector in on new targets." Fremont recently closed a non-brokered private placement for gross proceeds of CA$2 million. The initial offering was doubled when Palisades Goldcorp Ltd. came in with the lead order. Proceeds are going to be used for drilling at North Carlin, the exploration program at Cobb Creek and for general working capital. Analyst Thibaut Lepouttre wrote in Caesars Report on November 6, "Fremont Gold Ltd. has now closed the CA$0.05 financing, and the company ended up raising CA$2M after upsizing the original CA$1M placement. . .the CA$2M cash injection will fund the upcoming North Carlin drill program where the company is planning to drill three holes for a total of 1,500m. . .Fremont should be able to end the year with a strong treasury while waiting for the North Carlin assay results." James Kwantes noted in Resource Opportunities on October 11, "Fremont Gold Ltd. is pivoting to its 42 sq km North Carlin project. The company is permitting 10 drill sites and plans to drill about 1,500m at North Carlin, a deeper target, in the next couple of months." Fremont has 122.9 million shares outstanding, 201.4 million fully diluted. Read what other experts are saying about: Disclosure: Additional disclosures: Caesars Report: Disclosures from Resource Opportunities

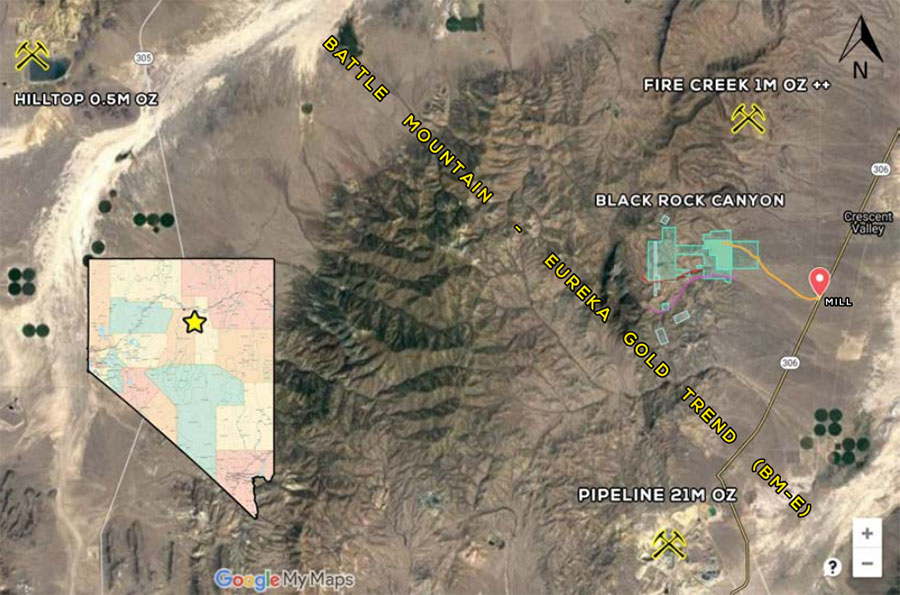

( Companies Mentioned: FRE:TSX.V; FRERF:OTCQB; FR2:FSE, ) from https://www.streetwisereports.com/article/2020/11/12/explorer-puts-focus-on-north-carlin-project.html Source: Streetwise Reports 11/12/2020 Cyon Exploration's project, in "Elephant Country," near the huge Cortez mining complex, offers the potential of both placer and hard-rock mining.Nevada's Cortez Trend is home to mega deposits, such as the Barrick Gold-Newmont JV Pipeline-Cortez complex that is estimated to have 45 million ounces of gold. Newly renamed Cyon Exploration Ltd. (CYON:TSX.V)—formerly True Grit Resources—recently acquired the Black Rock Canyon property, located also in the Cortez Trend, lies not far from this behemoth of a mine. "Carlin-type gold deposits that run through the Pipeline-Cortez mining complex are indicated to head directly through Black Rock Canyon," Byron Coulthard, Cyon's president and CEO, told Streetwise Reports. And the company aims to find out if it does. The nearly 3,900-acre property has seen some barite and gold placer mining in the 1980s and 1990s. The property had been leased to various exploration companies, and over the years a lot of surface sampling for placer gold as well as shallow drilling was done. "The aim of the drilling was to look for shallow bulk machinable, open pit deposits, something that they could heap leach quickly," Coulthard said. Historical surface samples returned assays that ranged from 2.02 grams per tonne (g/t) gold to 109.7 g/t gold. Geologist Steven Weiss, technical advisor to Cyon, told Streetwise Reports that some of the shallow holes "intersected 600 feet of low grade gold that averaged 0.1 g/t, which is not anything economic, but it indicates a significant amount of gold in fluid leakage into the rocks in that part of the property. Those rocks are not good host rocks, but beneath those formations at depth we have very good regional evidence for much more prospective rocks called the Roberts Mountains formation and the windband limestone." "Whenever there's a good gold anomaly in the rocks above the Roberts Mountains formation, it's of a lot of interest for finding a potential high-grade portion of a Carlin-type gold deposit or a skarn deposit down in the Roberts Mountains or the windband formations," Weiss said. Coulthard noted that Cyon recently purchased a lot of airborne data that it is overlaying on its map. "Because we have so much historical data, we do not need to spend a lot of time and effort trench sampling." On November 4, Cyon announced that it has compiled and is analyzing the historical data to select the best sites for deep drilling. "With only shallow drilling completed on the property historically, the topography suggests that the Cortez gold trend dips to a deeper depth and drilling to over 1,100 feet is needed," the company noted. Coulthard explained that the Black Rock Canyon property is situated in an extremely prospective area. "This property lies in a region where there are some really large, productive gold deposits and gold mines. Off to the southeast are the Pipeline and Cortez deposits, which are being mined by the Barrick Gold JV. And off to the northwest is the Battle Mountain district, where Newmont is busy mining at the Phoenix deposit. Just a few miles directly west of the property is a place called the Hilltop Mine, which was a historical gold producer. So the Black Rock Canyon property is in a really productive and prospective address."

Cyon also recently acquired the Aspen Gold Property in northern British Columbia. The property is situated about 25 kilometers from Artemis Gold's Blackwater Gold Project that has a Measured and Indicated resource of 12.4 gold equivalent ounces. Artemis just released an economic impact study on the project that estimated the Blackwater gold project would serve as a new economic engine for central British Columbia and Canada, contributing more than CA$13.2 billion to its economy over a period of 23 years. Cyon's Aspen project is made up of 16 mineral claims over 7,450 acres. Forest service roads provide direct access. Initially, Cyon plans to update Aspen's existing 43-101 report. "Based on that, we will decide how to proceed," Coulthard said. "We will conduct an induced polarization survey and some aerial work in the spring." Cyon has 46 million shares issued, 64 million fully diluted. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure:

( Companies Mentioned: CYON:TSX.V, ) from https://www.streetwisereports.com/article/2020/11/12/will-going-deep-on-cortez-trend-property-in-nevada-uncover-bonanza-grade-gold.html Source: Maurice Jackson for Streetwise Reports 11/11/2020 In conversation with Maurice Jackson of Proven and Probable, Michael Rowley, the CEO of Group Ten Metals, outlines the latest developments at the company's flagship project.Image Taken from Stillwater West Maurice Jackson: Joining us for a conversation is Michael Rowley, the CEO of Group Ten Metals Inc. (PGE:TSX.V; PGEZF:OTCQB; 5D32:FSE). Mr. Rowley, glad to speak with you, sir, to get us up to date on the latest, exciting developments on the high-grade, polymetallic Stillwater West project located in Montana. Before we begin, Mr. Rowley, please introduce us to Group Ten Metals and the opportunity before us.

Michael Rowley: Group Ten Metals is a growth-stage exploration company. We are pre-resource and we are about to debut three resources at our flagship Stillwater West project. In total, we have three district-scale assets. Two of these are PGE-nickel-copper. One of them is high-grade gold and the two of them, one of the PGE [platinum group element] projects and the gold project, are effectively for sale, at this point, to focus on the Stillwater Project, which is what we'll focus on today.

The Stillwater West Project is a remarkable opportunity. We got it in 2017 and quickly advanced it based on the database. We drilled it in 2019 and we just completed additional drilling a matter of weeks ago, and those results are pending. The potential that we see there, and our focus, is on proving up what we see as a Platreef potential.

We're completing a process that started in the 1970s, when previous work in the Stillwater District and the Stillwater Igneous Complex was dedicated for platinum, when America needed catalytic converters. They took parallels from the Bushveld District of South Africa, which is the source of most of the world's platinum, and they found the J-M reef deposit, which is actually in the exact same place in the stratigraphic layers at Stillwater, as it is at Bushveld in the parallel system.

Now, what's interesting is that the Bushveld went ahead with the development of these massive nickel-copper-sulfide-PGE mines in the lower portion of the Bushveld Complex in the 1990s. That was never continued in Montana, even though the parallels were fairly well known and were even talked about in technical papers. So, in a sense, we're just completing that example. We're just completing that process and bringing that thinking back to Stillwater West from a known comparable system in South Africa. Maurice Jackson: Group Ten Metals has been working very meticulously on the Stillwater West, as the company continues to demonstrate its proof of concept. The results to date, as with each press release, have been nothing short of exceptional, and what appears, as you referenced, to be the next major Platreef discovery. Mr. Rowley, Group Ten has just announced the completion of mapping and sampling yielding what has been a recurring theme, more high-grade results on platinum and palladium. Also, your latest release discussed a very large induced polarization survey conducted on the property. Take us to the Stillwater West and provide us with some context on what these early results from your 2020 program may indicate.

Michael Rowley: Group Ten had a fantastic year on the ground at the Stillwater West. We began early in the year with some studies based on drill core at the shack. We moved out in the field in April and May. You've got those results already from the earlier stage targets that we identified in the soil survey we did last year—some very high-grade results in those early areas. We then moved to bigger programs at the most advanced target areas, and that's key to our strategy. We have a lot of targets, so we're focused on converting known mineralization at those three most advanced target areas to our first formal resources of the project, and then on expanding that drill to find mineralization into these untested adjacent highs that you can see in our figures. So we're looking for both grade and scale here, and that's been the priority in our work, and we're blessed in terms of our database that we're starting on second, or even third base, in terms of getting there. In this year's program—our biggest yet—we drilled five holes, totaling more than 1,800 meters, in the Chrome Mountain target area. That's in addition to drilling that we did at Camp and HGR, the other two most advanced target areas last year. In all three cases, we're driving the exploration models and expanding known mineralization. We now have more than 31,000 meters of drill data, and we're on track to debut our maiden resources early next year.

I'll just maybe throw in a little bit about that Platreef-style target because, as mentioned, it's the Mogalakwena and Ivanhoe Platreef model from South Africa. So these are big, disseminated sulfide systems—nickel and copper sulfides—tens and hundreds of meters thick and kilometers long and rich in PGEs and also gold. We also see cobalt in a system at Stillwater, which is something they don't have in the Bushveld. Maurice Jackson: Michael, the global demand for clean air is on the rise, with an obvious explosion in demand for electric vehicles, battery storage, fuel cells and so much more, that the US government has been prompted to add a number of your commodities on the critical metals list. In other words, these are mineral commodities that are vital to the nation's security and economic prosperity. The Stillwater West is a polymetallic and a potential source of several of these battery-grade metals, such as nickel, copper and cobalt. What can you share with us?

Michael Rowley: The Stillwater West is fundamentally a nickel-and-copper sulfide system. That is the Platreef model. It's enriched in PGEs and cobalt and gold as well. Specific to nickel, battery-grade nickel is nickel sulfide, so we have what Tesla and the other EV [electric vehicle] companies are looking for. There are very few projects with potential for grade and scale in the world in this regard. There are not many magmatic systems out there of any size. Group Ten shares one of the largest and best geological formations in the world, the Stillwater Igneous Complex, with the major producer, our neighbor, Sibanye Gold Ltd. (SBGL:NYSE). They operate three mines right beside us, and they have a smelter refinery complex in the district. Their mines are the highest grade of the type in the world, whopping 80 million ounces of palladium and platinum, and more than half an ounce per tonne grade. So there's a lot of metal in this system and that has to speak well for our chances as we get into that lower portion of the system. In addition to nickel, the U.S. has listed PGEs, such as palladium, platinum and rhodium, as critical, and also cobalt. That's to secure domestic supplies and reduce dependency on Africa and Russia and other countries for supply. So we're not only in some of the very best rocks in the world for these target commodities. We happen to also be in a U.S. district that is a producing mining district, and that has to be beneficial for Group Ten. Maurice Jackson: You somewhat alluded to it, but you also have the infrastructure that is paramount to the success of this story as well. Michael Rowley: Absolutely. Our neighbor is mining just a few hundred meters north of one of our target areas. Maurice Jackson: Michael, to date, each press release has been a complete success in my view. Tell us more about the results to date on the other precious metals that make up the portfolio, beginning with gold and then rhodium. What have you discovered on the Stillwater West? Michael Rowley: Gold is a good one to discuss, because we have it broadly in that Platreef-style basket across the 25-kilometer span of the project. So, by co-product, I mean it's at co-product levels. Our value split at Stillwater is probably a third nickel, a third palladium, and then a third the other, and gold is in that other basket. But we do have one area of high-grade gold at Stillwater, which is running more than 8 grams per tonne. It's a nice grade. It's drilled in the 1980s, drilled in the 2000s. We've block-modeled it there. It's not a resource that we can advance immediately this year. We are working on it, and I think we'll bring that to the table in the future. It is open for expansion, and our work with the soils, in particular, showed high-grade gold in soils two kilometers to the west of the drill-defined high-grade gold at the Pine target. So there's some very good expansion potential there. We also identified similar levels of gold 9 kilometers away in the magmatic layers of the HDR target. So we've got a new model, a new understanding of gold mineralization at Stillwater here that's very exciting, and takes it away from what was thought to previously being contained to a shear zone. We're looking forward to reporting more on that. We did some good work on that this year. Rhodium is very strategic, as there is essentially no mine supply in North America to speak of—it's very little. Earlier this year we announced, I think we talked about it in one of our interviews previously, we show good rhodium co-product values across some size, and that would be immensely strategic in North America. Rhodium, I think you just said it, is $14,000 per ounce today. It's back up; it's high. And, like palladium, that's due to persistent supply deficits year after year. Maurice Jackson: What kind of grams are we looking at from the previous press releases? Was it about 6-7 grams per tonne, somewhere in that range? Michael Rowley: We chipped a rock that was nearly 6 grams per tonne rhodium, which is the highest I've seen, and that certainly speaks to the potential for grade. The highest grade rhodium mine in the world is less than half a gram per tonne, so it's rarely at those high levels. That's the UG2 Reef in the Bushveld, South Africa. The great majority of other rhodium producers are running at 0.1 grams, even sometimes 0.2 grams per tonne, and that's the range that we're seeing in those results reported in drill core. Maurice Jackson: Now I would be remiss if I didn't ask this two-part question. When can shareholders expect the maiden resource to be published? And where do you think it will put you in relation to your peers? Michael Rowley: We have block models developing on five target areas. Those are presented very nicely in our materials. The focus is on the most advanced three, and those are the Discovery Camp and HGR areas. They've got the most drilling, and it's holding together really nicely in terms of continuity and grade. We're going to incorporate this year's drill results and then do our best to get them out quickly. So we're looking, I think, at an early 2021 release date, and we're looking forward to providing more details on that. In terms of our peers, it's hard to find a direct fit and, of course, we do not have published numbers to talk about yet. But in broad terms, if you look at our current peers, we have the PGEs that, say, a Generation Mining Ltd. (GENM:TSX; GENMF:OTCQB; 9GN:FSE) has, but we also have nickel that they don't have. I guess another point that separates us is that we own our asset 100%, and they have a 51% interest to date. Another peer might be Canada Nickel (CNIKF:OTCMKTS), but again, it's not a direct comparison, as they have limited PGEs so far. If you could just blend those two in terms of geology, then you're getting somewhere closer to the Platreef model that we're looking at, which is Ivanhoe Mines Ltd.'s (IVN:TSX; IVPAF:OTCQX) Platreef Line in South Africa. Maurice Jackson: Leaving Montana and moving onto Ontario, Group Ten has a portfolio of projects, any of which could be a flagship for an explorer. With gold resuming an upward trajectory, update us on the Black Lake-Drayton Project in Ontario, Canada, sir.

Michael Rowley: Very interesting things happening in the district out there. Treasury Metals Inc. (TML:TSX: TSRMF:OTCQB) has done a fantastic job of consolidating the rest of the district. They've purchased effectively the Goldlund deposit so they now have, between their Goliath and Goldlund now consolidated, they have over 3 million ounces and a permit to build a mill. That's one of the largest undeveloped gold projects in Canada and North America. It's very attractive. That's right beside a highway, power, all that good stuff. We share the district with them. We have the remaining one-third of the district. We have all the same geology, 127 holes in the database. We're getting a lot of interest in this asset now from some very good parties. I think that reflects the move in gold that you mentioned, and also a quickly accelerating M&A environment. So I'm optimistic to see what we can do in that regard. Our objective here would just be to get some value for it. We're not getting anything, I think, on our balance sheet at present for it, yet it's a really good project. We'd be glad to have a very good share position in the gold space, for example, and let somebody else advance it so we can focus on Montana. Maurice Jackson: Should that come to fruition that would be great for organic growth and no more shareholder dilution without any financing down the road. Michael Rowley: Absolutely! Maurice Jackson: Switching gears, sir, please provide us with an update on the current capital structure for Group Ten Metals.

Michael Rowley: We have about 145 million shares out at present. Our prices just moved up nicely the past few days. We're about a $50 million market cap, I think. I haven't calculated it recently. A key point is that we have $4 million in the treasury and we have $11 million in the money warrants. So we are presently funded through everything we need to do this year and potentially even next year if you assume those warrants come in. We do have some key news events on the horizon that are going to drive price, and that would be drill results, which we expect to start receiving shortly. That will be ongoing over the next couple of months. The final results from that IP survey, which was fantastic, I think people can look forward to some updated promotional materials with lovely pink images from that survey and, of course, the resources, ultimately, in the new year at some point, and those would be major catalysts. I don't think we'll have to do a placement before then. We are in some very good discussions with some big players in the industry. If, on the right terms, we see the right opportunity to bring a strategic partner in, we will do that. But so far, we see a lot of value we can add here as well before we look at further placements. Maurice Jackson: Last question, sir. What did I forget to ask? Michael Rowley: We should probably touch quickly on the Yukon, the Kluane Project, as our neighbor Nickel Creek Platinum (NCP:TSE) has a new CEO. That deposit, formerly known as the Wellgreen Deposit, now the Nickel Shaw Deposit, they seem to be putting some attention to again. It's a great district. This is one of the largest undeveloped nickel-copper-PGE deposits in the world. The whole Kluane Belt is good and we, of course, are the largest landholder in that belt. We currently have some interest in one project of the four that we own in that group, and I think we'll see that accelerate in the coming weeks and months. Maurice Jackson: Mr. Rowley, if someone listening today wants to get more information on Group Ten Metals, please share the website address. Michael Rowley: www.grouptenmetals.com Maurice Jackson: Mr. Rowley, it's always a pleasure to speak with you, sir. Wishing you and Group Ten Metals the absolute best. Before you make your next bullion purchase make sure you contact me. I’m a licensed representative to buy and sell physical precious metals through Miles Franklin Precious Metals Investments where we offer a number of options to expand your precious metals portfolio from physical delivery of gold, silver, platinum, palladium and rhodium directly to your home or office, to offshore depositories and precious metal IRAs. Call me directly at (855) 505-1900 or email [email protected]. Finally, please subscribe to Proven and Probable, where we provide mining insights and bullion sales. Subscription is free. Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure: Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734. The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk. Images provided by the author.

( Companies Mentioned: PGE:TSX.V; PGEZF:OTCQB; 5D32:FSE, ) from https://www.streetwisereports.com/article/2020/11/11/explorer-anticipates-platreef-potential-drill-results-from-montana-prospect.html Source: Peter Krauth for Streetwise Reports 11/09/2020 Peter Krauth looks into what Pfizer and BioNTech's COVID-19 vaccine efficacy announcement could mean for gold and silver.Believe it or not, the big deal for precious metals this week was not the U.S. election. It was news that Pfizer and BioNTech's COVID-19 vaccine was over 90% effective in preventing the virus, and would likely be among the first to receive FDA authorization. Monday was massively risk-on, with the Dow soaring 4% to a new record high, ten-year treasuries yields shot up almost 17% in a single day as investors dumped bonds, and oil was ahead 8%. Meanwhile, the U.S. dollar index gained about 60 basis points or 0.65%, while higher-beta currencies jumped. Gold and silver both sold off quite strongly and stayed near their lower price levels. Naturally, some gold and silver enthusiasts are asking themselves if a vaccine is enough to kill the Covid-19 virus, as well as the precious metals bull market. And based on the initial reaction of these metals, it's a natural question. So let's look at the implications. Is the Gold and Silver Party Over? The encouraging news everyone's been waiting for appears to finally be here. We're getting a glimpse of light from the end of this long tunnel. As a result, gold dropped $84 or 4.3%, while silver lost 5.3%, on this news. But is this a sign of things to come, or a knee-jerk reaction that's just short sighted?

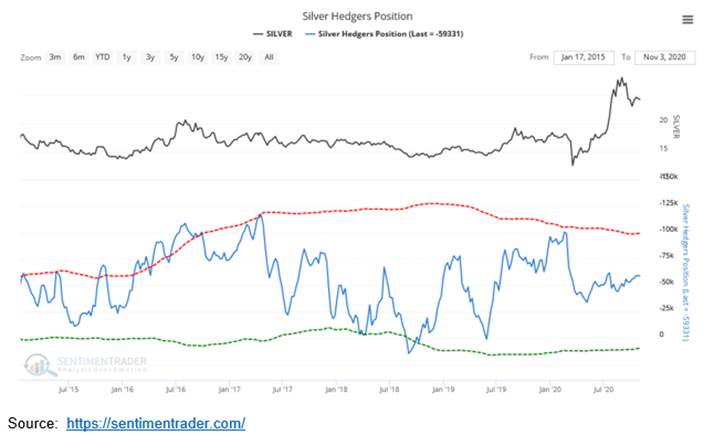

Although highly positive and very reassuring, the truth is we're not going to be lining up tomorrow to get our first of two doses of Pfizer's vaccine. The road to normalcy, whatever that will mean, is still a long one. Consider that Pfizer expects to only produce 50 million doses this year, and up to 1.3 billion in 2021. Logistics will be a challenge, as the vaccine will need to be stored at -70 degrees Celsius, which is much colder than other vaccines. Storage, transportation, logistics, security and prioritization will all be complex. The first to receive the vaccine will be higher risk people and healthcare providers. Two doses, 21 days apart, are required. Basically, it's going to take quite some time to get this vaccine rolled out and administered even in developed nations. Imagine for a moment what that might look like in developing ones. That could keep travel and other sectors that can't easily implement social distancing from recovering early. And I've barely scratched the surface of challenges brought on by a vaccine roll-out. The Solution May Only Exacerbate Things Realistically, COVID-19 is a long way from being a distant memory. Restricted movement, quiet cities, empty restaurants, cinemas and gyms, and mostly local tourism. Daily life will continue to trudge forward. Unfortunately, that also includes the world's ongoing geopolitical tensions. I don't see relations between the two biggest economies, the U.S. and China, cozying up anytime soon, as both sides want to continue "looking tough." We know the Fed has promised to keep rates near zero through 2023 to support economic recovery. It also vowed to let inflation "run hot" above 2% to make up for years of anemic levels. Debts and deficits are going to continue to soar. Even with a Republican-led Senate, Biden's still likely to get a $500 billion to $1 trillion "skinny stimulus" bill passed early next year. Though well under the $3 trillion bill passed in May, Goldman Sachs says this would still be nearly 5% of GDP. Gold and Silver Still Strong In my view, gold and silver simply had not finished correcting after gold established an all-time record high in August. Sentiment is a tricky market driver to navigate. But one thing is fairly clear, gold and silver hedgers (smart money) have not yet flipped to a bullish stance.

They remain cautious right now on gold.

And as for silver, they appear to be stuck in neutral. If anything, the sell-off may be the catalyst many have been waiting for to help gold and silver establish a bottom, or at least an end to their consolidation. I believe Pfizer's positive vaccine news may only have dented precious metals for a short time, as it scared some weak hands out of the sector. Odds are smart money is going to start buying the dips and accumulate gold and silver, as it gears up for the next, inevitable rally. After all, it's going to take a lot more than a vaccine that kills COVID-19 to also kill gold and silver. --Peter Krauth Peter Krauth is a former portfolio adviser and a 20-year veteran of the resource market, with special expertise in energy, metals and mining stocks. He has been editor of a widely circulated resource newsletter, and contributed numerous articles to Kitco.com, BNN Bloomberg and the Financial Post. Krauth holds a Master of Business Administration from McGill University and is headquartered in resource-rich Canada. Sign up for our FREE newsletter at: www.streetwisereports.com/get-newsDisclosure:  from https://www.streetwisereports.com/article/2020/11/09/can-a-covid-vaccine-kill-silver-and-gold.html Source: Streetwise Reports 11/06/2020 The investment case for Nomad Royalty Company is made in a Velocity Trade Capital report.In a July 7 report, analyst Michael Siperco reported that Velocity Trade Capital initiated coverage on a new royalty entrant, Nomad Royalty Company Ltd. (NSR:TSX; NSRXF:OTCQX), with an Outperform rating and a CA$2.25 target price. In comparison, Nomad is trading at about CA$1.41 per share. "Nomad offers a pure play, precious metals royalty portfolio at a discount to peers, focused on near term cash flow and return, with rerate and growth potential that rivals producers in a higher margin, more diversified, lower risk investment," Siperco added. The analyst presented the key points about Nomad. One, the company, founded earlier this year, began with a "strong initial base of cash generating assets." Of its 10 assets, four are royalties, four are streams, one is a gold loan and one is a future contingent payment. Five assets are currently producing, and another two are expected to begin doing so in 2021. "By YE2021, without additional transactions, we expect Nomad to be at about a 25,000 ounce per annum run rate, generating +US$30 million per year in free cash flow at spot metal prices," Siperco indicated. Two, the company is expected to aggressively pursue further deals. Management is willing to consider a vast array of potential transactions in terms of jurisdiction, commodity type and structure, including partnerships, syndication, and perhaps even mergers and acquisitions. "We see additional transactions, portfolio acquisitions and diversification driving dividend growth and multiple rerating over time, even as organic delivery/cash flow growth accelerates into 2021," commented Siperco. Three, Nomad's top executives and co-founders, Vincent Metcalfe (CEO), Joseph de la Plante (chief investment officer) and Elif Levesque (chief financial officer), have had great success in the past, having expanded Osisko Royalties' portfolio to more than 100-plus from one, in about five years' time. "We have a high degree of confidence in management's ability to source new transactions and effectively manage the growth of the company," Siperco noted. Four, Nomad's management team is focused on cash flow and returning cash to shareholders. For instance, it is looking at instituting a dividend policy. Five, Nomad offers investors low-risk leverage to metal prices and value. "While a gold-silver bull market may lead to higher torque among producers, the upside from a lower risk, rapidly growing, production-focused new entrant should be highly attractive," Siperco purported. Six, though Nomad is currently trading lower than the rest of the companies in the royalty and streaming sector, that is expected to change. "We see additional transactions, portfolio acquisitions and diversification driving dividend growth and multiple rerating over time, even as organic delivery/cash flow growth accelerates into 2021," Serpico wrote. Read what other experts are saying about: Disclosure: Disclosures from Velocity Trade Capital, Nomad Royalty Company Ltd., July 7, 2020 I, Michael Siperco, hereby certify that all of the views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. I receive compensation from Velocity that is based upon various factors including Velocity total revenues, a portion of which are generated by Velocity Investment Banking activities. Velocity has established and implemented written policies and procedures to minimize conflicts of interest between its Clients and Velocity and its Analysts. Velocity does not allow its Analyst or household family members to hold or trade in any security on which the Analyst writes research reports. Other than what is disclosed below, Velocity is not aware of any material conflict of interest between itself and its Analyst and the Firm’s Clients. No employee, officer or director of Velocity is a director, officer or employee of the issuer or has received remuneration from the issuer, other than normal course investment advisory or trade execution services in the last 12 months. As with all employees of Velocity, a portion of the Analyst’s compensation may be derived from Investment Banking earnings. The Analyst does not receive any direct compensation from Investment Banking fees received from this issuer. Company-Specific Disclosures:

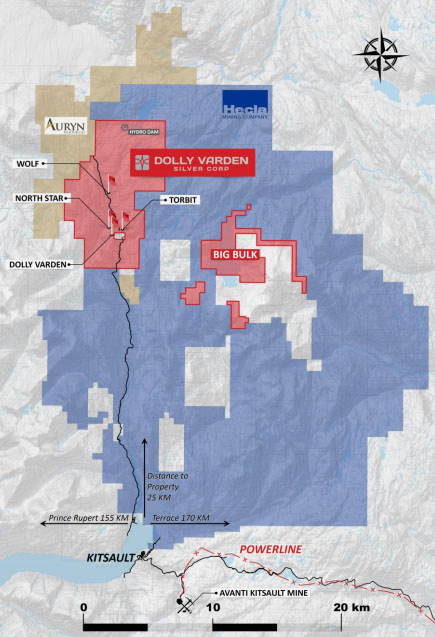

( Companies Mentioned: NSR:TSX; NSRXF:OTCQX, ) from https://www.streetwisereports.com/article/2020/11/06/coverage-initiated-on-royalty-firm-growing-cash-flow-at-the-right-price.html Source: Streetwise Reports 11/05/2020 Dolly Varden Silver is discovering new high-grade silver deposits on its property where silver mining began 100 years ago.It's called the Golden Triangle, but it's home to lots of silver too. Dolly Varden Silver Corp.'s (DV:TSX.V; DOLLF:OTCMKTS) large Dolly Varden property in northwest British Columbia has a long and storied history. The Dolly Varden/North Star Mine operated only for a few years, from 1919 until 1921, but in that short interval produced 1.3 million ounces of silver at an average grade of 1,109 grams per tonne (g/t). Several decades later, the Torbrit Mine operated from 1949 through 1959, and produced 18 million ounces of silver, with an average grade of 466.3 g/t.

Production ceased at the Torbrit Mine in 1959, Dolly Varden President and CEO Shawn Khunkhun told Streetwise Reports, because of the low silver price, 85 cents per ounce. "And a lot of the deposit was left intact." Dolly Varden has been quantifying that silver. The company drilled more than 55,000 meters in 174 holes from 2017 to 2019, making new discoveries and expanding the resource. The updated mineral resource estimate released in May 2019 calculated 32.9 million ounces of silver Indicated and 11.4 million ounces of silver Inferred. Shawn Khunkhun took the helm of the company in February of this year. "At that time, Dolly Varden was trading well below its peers. The first thing I did was bring in a team of regional experts," he said. "Mining areas can be very dissimilar. Nevada, Ontario's Red Lake, South Africa are all very different from each other; operating in these disparate jurisdictions takes a certain type of skill set. There are nuances in the Golden Triangle, so I brought in a technical team—exploration geologists, mining engineers, miners—that had regional expertise." Khunkhun also focused on building a foundation of shareholder support. "Eric Sprott, who was a shareholder in the company, took a bigger stake, growing his interest to 19.9%. Hecla Mining operates the Greens Creek silver mine in Alaska just outside of Juneau that may be analogous to our project. Hecla has been a shareholder and in 2016 tried to take over Dolly Varden. Hecla has supported the new management team by investing about $2 million this year and now has about a 12% stake." Khunkhun noted that positioning Dolly Varden as a "high-grade silver company in a safe jurisdiction, backed by Eric Sprott and Hecla Mining, caught the interest of a lot of silver-focused shareholders. We immediately went from trading at half the value of our peers, to trading in line with them." This summer the price of silver broke out, and with that the market cap of silver companies also increased. "We took advantage of that to raise around CA$20 million," Khunkhun said, "so now we are in a great cash position." This year, Dolly Varden initiated a 10,000-meter exploration program, focused on growing the Torbrit deposit. On October 7, the company announced stepout drilling assays as high as 351 g/t silver over 12.75 meters, including 1083 g/t silver over 2.70 meters, and 135 g/t silver over 37.50 meters, including 906 g/t silver over 1.00 meter. In-fill drilling returned assays as high as 302 g/t silver over 31.95 meters, including 642 g/t silver over 4.00 meters. "We are pleased to see step out drill intercepts with consistent, strong silver mineralization, significant thickness, and areas of very high-grade silver," Khunkhun said. "These results should support continued resource expansion and the growing potential for bulk underground mining around the past-producing Torbrit Silver Mine." Dolly Varden has two rigs working on the property, "and we've got a tremendous amount of drilling to report," Khunkhun said. The rising price of silver may change the plan for Dolly Varden. "When I took over, the company had 44 million ounces of silver in the ground, in a modern 43-101 resource estimate from 2019. At $17/oz silver, there's a certain net present value to that. But once you start looking at where spot silver prices are today, I'm now looking at Dolly Varden through a different lens. I'm now looking at it as a potential development story," Khunkhun explained. Khunkhun sees the potential for a regional play. "Hecla Mining owns a huge concession of land and a mineral trend to the east of our property. On the other side of our property is Fury Gold Mines, which put out a preliminary economic assessment in April of 1 million ounces of gold and 20 million ounces of silver. Dolly Varden sits in the middle. This is really a regional opportunity. The economies of scale of the region make developing and making a production decision a lot more compelling than just one of these three pieces going alone." In addition to Dolly Varden's main silver property, to the east lies its Big Bulk copper-gold prospect. "The Dolly Varden property has some structural and stratigraphic similarities to Eskay Creek and Brucejack, two of the big mines in the area, while Big Bulk is more similar to the KSM or Red Chris porphyry deposits. So we have two projects in the area that cover both styles of mineralization—it's all highly prospective." Khunkhun explained. Khunkhun notes that the Dolly Varden project is a silver pure play. "Many silver companies put out their figures as silver equivalents, but if you look closely, you will see they may have a lot of zinc or lead. The silver price is soaring while zinc and lead are not accelerating in price at the same trajectory." "Dolly Varden has the potential to significantly grow its deposit; it offers the potential of M&A regionally or beyond," Khunkhun concluded. Dolly Varden has 121.96 million shares outstanding, 136.55 million fully diluted. Institutions such as U.S. Global Investors, Sprott Asset Management, and Ingalls and Snyder accounts account for 50%; Hecla Canada 11%, Eric Sprott 19.9% and insiders 5%. Analyst Stuart McDougall of Mackie Research covers Dolly Varden and rates the firm Speculative Buy, with a CA$1.00 share target price. The shares are currently trading at around CA$0.83. Read what other experts are saying about: Disclosure:

( Companies Mentioned: DV:TSX.V; DOLLF:OTCMKTS, ) from https://www.streetwisereports.com/article/2020/11/05/the-drill-bit-is-expanding-the-silver-resource-in-bcs-golden-triangle-project.html Source: Streetwise Reports 11/05/2020 The investment highlights of Nomad Royalty Company are presented in a Cormark Securities report.In an Aug. 20 report, analyst Nicolas Dion reported that Cormark Securities initiated coverage on precious metals royalty and streaming firm Nomad Royalty Company Ltd. (NSR:TSX; NSRXF:OTCQX), with a Buy rating and a CA$2.20 per share target price. The current share price is about CA$1.33. "As the portfolio scales up, we believe Nomad could rerate closer to its more senior peers," added Dion. The analyst explained the genesis of Nomad. Early in 2020, the three co-founders, Vincent Metcalfe, Joseph de la Plante and Elif Levesque, formed the company through a reverse takeover and vend-in of two royalty and streaming portfolios, one from Orion Mine Finance and one from Yamana. Today, Orion owns 77% of Nomad shares, and Yamana owns 13%. Nomad went public in May and subsequently acquired a 1% net smelter returns (NSR) royalty on the past-producing Troilus gold mine in Quebec. Nomad only invests in precious metals. Dion presented five key highlights of Nomad. The Montreal-based company is already generating cash flow. This is coming from its paying assets, Bonikro, Gualcamayo, RDM, Mercedes/South Arturo and the Premier gold loan, which account for 35% of its net asset value (NAV). Another two assets, comprising 41% of NAV, are slated to begin production in 2021: Blyvoor and Woodlawn. Other assets, including Troilus and Suruca, which make up 23% of NAV, are expected to come online over the next five years. "At spot prices, we expect $19 million in 2020 free cash flow and $31 million in 2021 free cash flow (before investments)," noted Dion. Nomad is considering a dividend of about CA$0.02 per year, which would be the highest among its peers. "The already strong free cash flow generation would more than support this," commented Dion. Nomad's executive team bring to the company, from their time at Osisko Royalties, experience in the royalty and streaming space. One of their goals is to reduce general and administrative expense to $4–5 million per year, which would be one of the lowest in its peer group. The company has a strong balance sheet, with $12 million in cash, no debt except the $10 million it owes Yamana and a $50 million revolving credit facility that it can increase to $75 million. "Nomad is well positioned to compete on royalty/stream transactions," Dion noted. Nomad has three major drivers of upside for shareholders, the analyst noted. One is multiple expansion as the company grows via acquisitions or projects advancing to production. Another is NAV growth through new deals and their inherent optionality. The third is higher precious metals prices. The report noted that potential stock moving events to watch for with Nomad are completion of the Blyvoor preliminary economic assessment due out in H2/20, operational updates concerning various projects and additional royalty/stream acquisitions. Read what other experts are saying about: Disclosure: Disclosures from Cormark Securities, Nomad Royalty Company Ltd., August 20, 2020 I, Nicholas Dion, hereby certify that the views expressed in this research report accurately reflect my personal views about the subject company(ies) and its (their) securities. I also certify that I have not been, and will not be receiving direct or indirect compensation in exchange for expressing the specific recommendation(s) in this report. The Disclosure Statement Chart for Nomad Royalty can be found on the website.

( Companies Mentioned: NSR:TSX; NSRXF:OTCQX, ) from https://www.streetwisereports.com/article/2020/11/05/coverage-initiated-on-new-midtier-royalty-company-with-cash-flow.html Source: Streetwise Reports 11/04/2020 The rationale for early buying into Nomad Royalty Company is explained in an iA Securities report.In a Sept. 23 research note, analyst Puneet Singh reported that iA Securities initiated coverage on Nomad Royalty Company Ltd. (NSR:TSX; NSRXF:OTCQX) with a Buy rating and a CA$2.30 per share target price. In comparison, Nomad is trading at about CA$1.24 per share. Singh explained why Nomad offers a ground floor investment opportunity for potentially immense rewards. First, the business model of this Quebec-headquartered company is "high margin, safe and proven at providing returns," the analyst indicated. Royalty firms offer safer gold exposure because they lack the capital and cost risks of traditional mining businesses. "Over time, most royalty firms have been able to return in excess of 25% CAGR since their inception," Singh noted. Second, producing or near producing assets already comprise the bulk of Nomad's net asset value (NAV). Producing assets account for 32% of NAV and include the Mercedes/South Arturo silver stream, the gold prepay loan, the Bonikro gold stream and the Riacho dos Machados royalty. Another 46% of NAV consists of near-term production assets, which include the Blyvoor gold stream and the Woodlawn silver stream. Those are scheduled to ramp up in 2021-2022. "By 2022, we estimate that Nomad will produce about 32,000 ounces of gold equivalent (i.e.,) up 87% on 2020E," Singh wrote. Third, Nomad has been "aggressively looking for new deals to add, from the onset," indicated Singh. Since going public in May, Nomad announced three deals. They are a 1% net smelter returns (NSR) royalty on the Troilus mine in Québec, a 1–3% NSR royalty on the operating Moss gold mine in Arizona and a 1–2.25% NSR royalty on the Robertson deposit in Nevada's Cortez Trend. "We would expect Nomad to continue to remain active trying to source new deals," Singh commented. Fourth, Nomad has the benefit of a management team that is experienced and adept at initiating, executing and closing royalty/streaming transactions. The company's three co-founders previously worked at Osisko Royalties and while there, expanded the entity from a single non-smelter returns royalty to where it is today. "Given management's track record and what they've done at Nomad so far, we think the team is well equipped and well versed to be competitive in a growing field of peers," noted Singh. He concluded his report with the recommendation that investors buy into Nomad now before it re-rates higher. History shows that those who bought a royalty company in its early days, Singh added, always got an excellent return on their investment. Already Nomad has initiated an annual dividend of C$0.02 per share. "As assets are added, diversification increases, and float (in top shareholders' best interest) and liquidity expand, Nomad will rerate higher," he purported. Read what other experts are saying about: Disclosure: Disclosures from iA Securities, Nomad Royalty Company Ltd., Initiating Coverage, September 23, 2020 Conflicts of Interest: The research analyst and or associates who prepared this report are compensated based upon (among other factors) the overall profitability of iA Securities, which may include the profitability of investment banking and related services. In the normal course of its business, iA Securities may provide financial advisory services for the issuers mentioned in this report. iA Securities may buy from or sell to customers the securities of issuers mentioned in this report on a principal basis. Analyst's Certification: Each iA Securities research analyst whose name appears on the front page of this research report hereby certifies that (i) the recommendations and opinions expressed in the research report accurately reflect the research analyst's personal views about the issuer and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii) no part of the research analyst's compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report. Analyst Trading: iA Securities permits analysts to own and trade in the securities and or the derivatives of the issuer under their research coverage, subject to the following restrictions. No trades can be executed in anticipation of coverage for a period of 30 days prior to the issuance of the report and 5 days after the dissemination of the report to our clients. For a change in recommendation, no trading is allowed for a period of 24 hours after the dissemination of such information to our clients. A transaction against an analyst's recommendation can only be executed for a reason unrelated to the outlook of the stock for the issuer and with the prior approval of the Director of Research and the Chief Compliance Officer.

( Companies Mentioned: NSR:TSX; NSRXF:OTCQX, ) from https://www.streetwisereports.com/article/2020/11/04/coverage-initiated-on-firm-with-proven-value-generating-royalty-business-model.html |

RSS Feed

RSS Feed